- Navigator

- Expansion Solutions

- Industry Analytics and Strategy

- Information Technology, Semiconductors, and AI

This article originally appeared in the February 2025 issue of Expansion Solutions magazine.

Digital information and content continue to grow across our daily lives and economy. This includes information and content related to streaming, coding, social media platforms, research, marketing, business services, personal services, health services, education, and more.

Additionally, artificial intelligence (AI) is creating new data and information at speeds much greater than ever before. This creates increased demand for the infrastructure and systems that move and store data, including data centers.

Regarding data center growth, JLL reports, “Data center demand is growing at an exponential rate, with data creation expected to increase at a 23% CAGR through 2030. Rising generative AI workloads have the greatest impact on data storage, followed by continued cloud and hyperscale growth. Investors are furthermore drawn to the sector by the sticky tenant proposition with high renewal probability.”

This article provides insights on the recent market, real estate, and investment trends in the data center industry and how critical factors like energy, land use, and local acceptance impact investment locations.

As reported by Cushman Wakefield, data center revenues have been experiencing annual growth, which is projected to continue. Furthermore, the projected demand is expected to be driven by AI.

2020: Total global revenues $91.7 billion

2028: Total global revenues $212.1 billion

Source: Cushman Wakefield

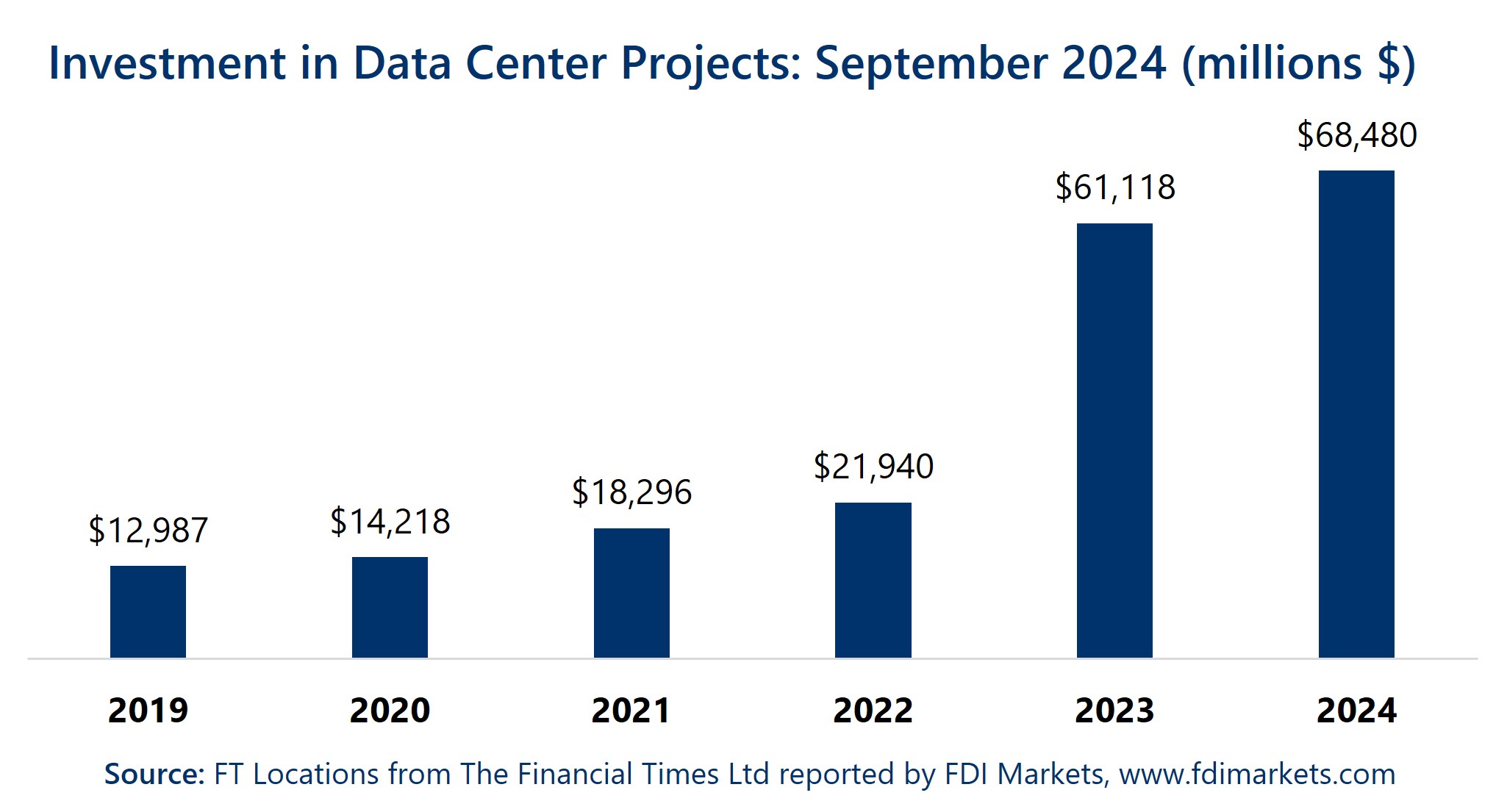

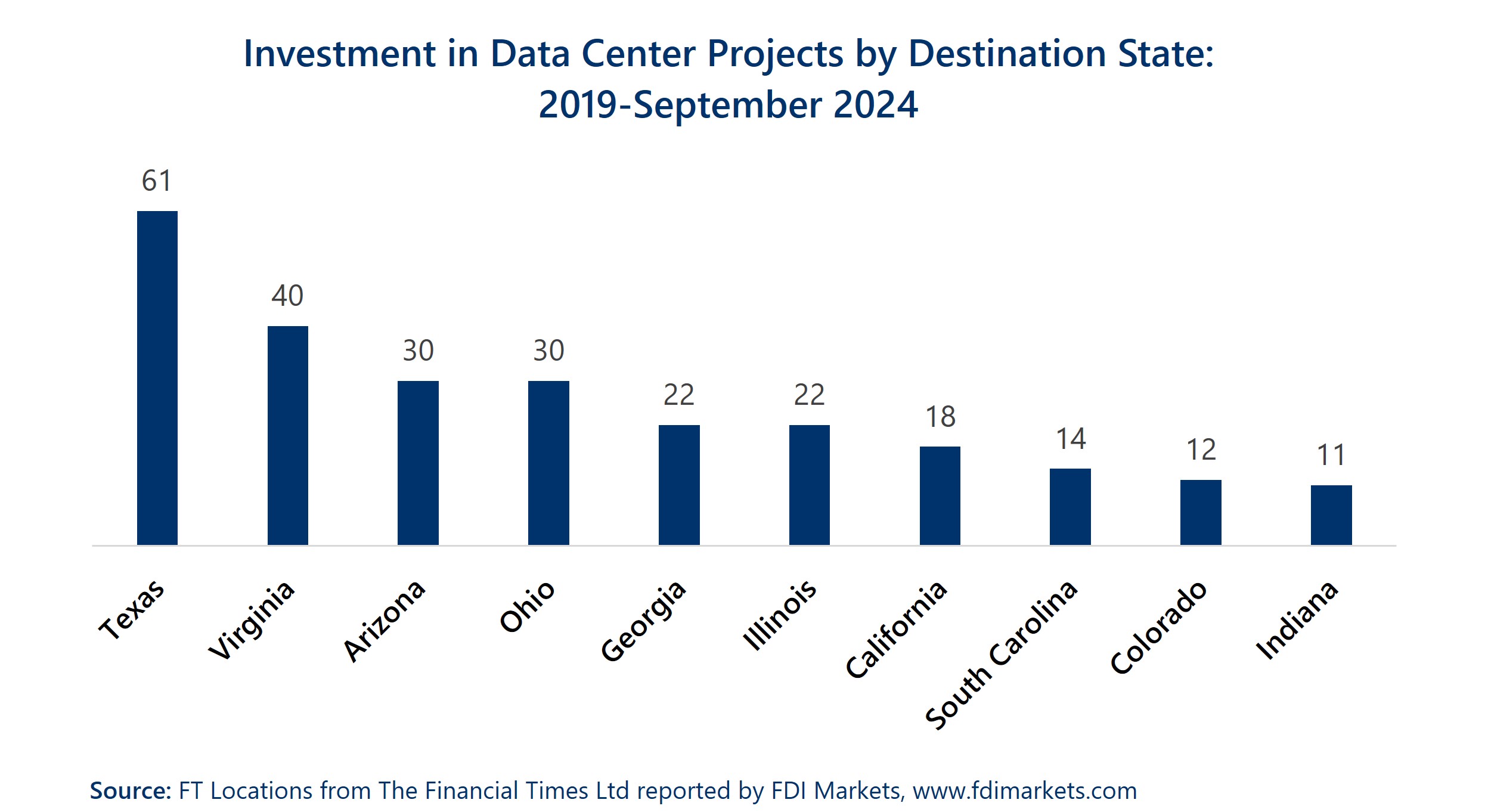

Investment trends mirror recent and projected growth in data center revenues. FDI Markets tracks investment and related data on data centers. Based on this data, Between 2019 and September 2024, for all projects invested in the US:

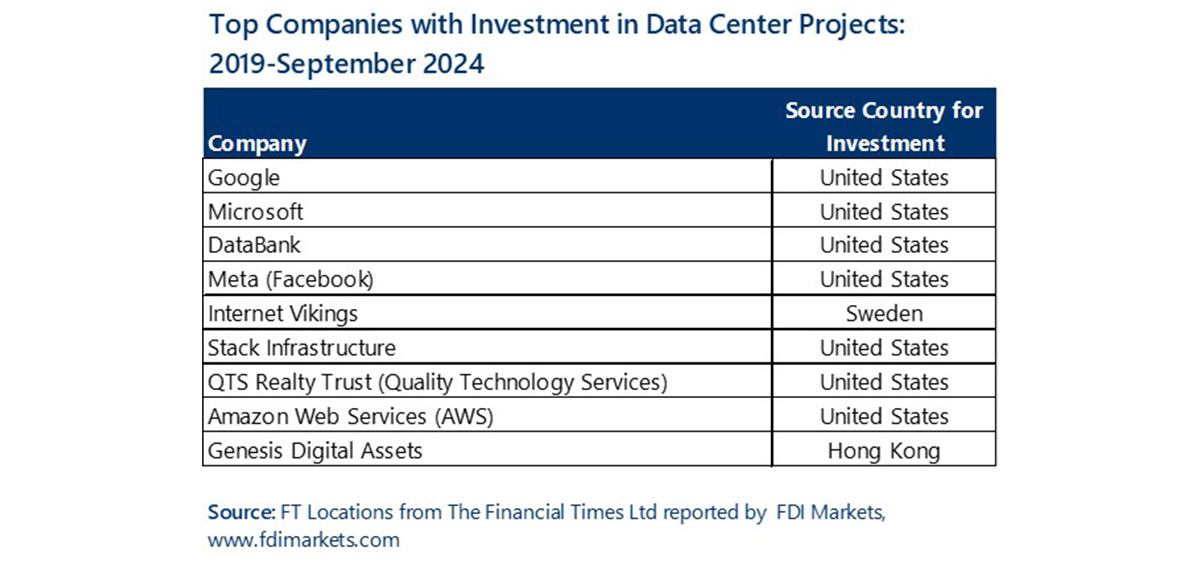

In terms of companies in which investment was made, the big tech companies (Google, Microsoft, Meta, and Amazon) were all at the top of the list, along with digital infrastructure and real estate companies.

In terms of companies in which investment was made, the big tech companies (Google, Microsoft, Meta, and Amazon) were all at the top of the list, along with digital infrastructure and real estate companies.

The increasing demand, revenues, and investment in data centers are creating opportunities for real estate development across the US and the Americas. Vacancy rates have decreased due to supply being constrained by longer project completion times and constrained energy supply while new capacity for energy is in the pipeline. Delays are also attributable to longer times needed for equipment and related supplies.

Regarding vacancy rates, CBRE reported that “… overall vacancy rate for primary markets fell to a record-low 2.8% in H1 2024 from 3.3% a year earlier, while the overall vacancy rate for secondary markets fell to 9.7% from 12.7% over the past year.” Similarly, Cushman Wakefield reports for 2024: “With power and component lead times constraining delivery of new supply, vacancy region-wide has fallen to 3%, driving over 80% of deliveries to be pre-leased in major markets and pushing lease rates higher.”

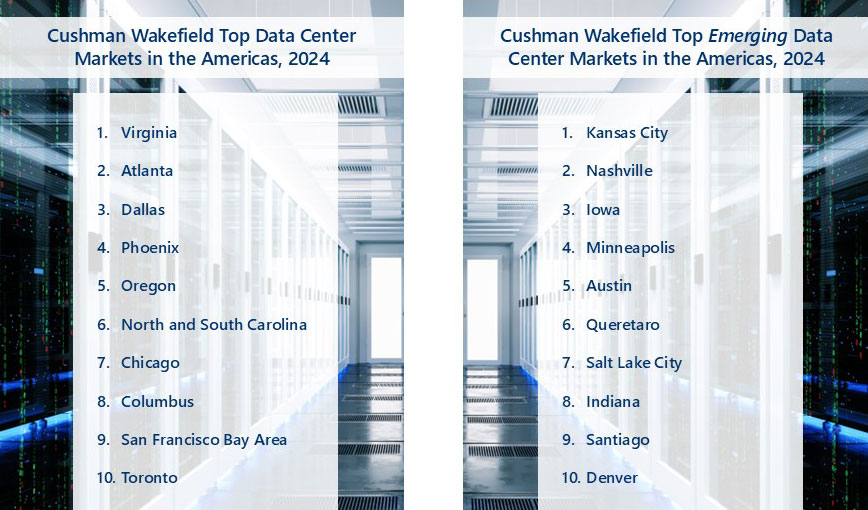

These trends result in investors and companies moving beyond the typical primary markets. Cushman Wakefield reports, “Interest in large-scale power availabilities, plentiful land and less strict latency requirements for AI, has driven hyperscalers and operators to expand in a host of historically peripheral markets such as Indianapolis, Kansas City, Reno, Charlotte, Salt Lake City, Minneapolis, Philadelphia, Montgomery, among many other outlying areas.” Putting all of the factors together, Cushman Wakefield produces a list of top ten and emerging markets.

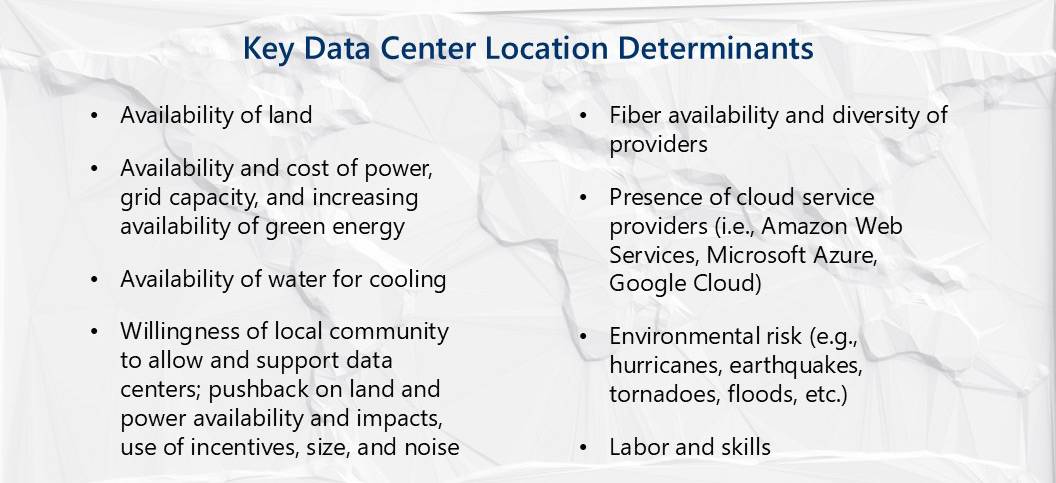

In attracting and supporting data center expansion and attraction, economic and business developers should assess their community and region in terms of critical factors that drive locations. Most importantly, this includes:

Both of these can best be answered and reflected in local and regional economic plans and strategies that article targeted goals and actions.

Regarding location factors and specifically workforce, economic and business developers often overlook the importance of labor because data centers are not seen as dense with workers per square foot of space.

Regarding location factors and specifically workforce, economic and business developers often overlook the importance of labor because data centers are not seen as dense with workers per square foot of space.

However, workforce and skill gaps are impacting every industry, and a recent JLL report found, “Finding the right talent remains a challenge for data center operators, and the issue is becoming more acute given the rapid expansion of the sector in recent years. Roles in the industry can be highly technical in nature, given the complexity of data center operations. Data center development is also expanding into rural areas with limited labor pools, presenting a unique set of staffing challenges. Given the technical nature of the data center industry, only about 15% of applicants meet the minimum job qualifications. Consequently, positions can often take 60 days or more to fill. Due to these hiring challenges, it is estimated that 10% of data center roles at existing facilities are unfilled, more than twice the national average across all industries.”

A key takeaway for economic and business developers interested in data centers is to be prepared. Markets and economic dynamics for data centers are changing rapidly along with technology. Therefore, success in supporting and attracting investment typically requires local and regional expertise and a commitment to prioritizing them as an ongoing target.

Camoin Associates is a trusted economic development and business prospecting consulting firm that helps communities and organizations achieve sustainable and equitable growth through expert analysis, effective strategies, and intentional connections.

By providing valuable insights, best-in-class data, and personalized, actionable strategies, we empower our clients to make well-informed decisions that drive economic success and foster strong, competitive markets.

Economic and Fiscal Impact Analysis

A recent analysis of a digital equity program in Westchester County, NY, revealed that it generated outsized economic benefits and return on investment for the community.

Business Retention and Expansion (BRE)

Industry Analytics and Strategy

Your resource for understanding today and looking toward tomorrow