- Navigator

- Expansion Solutions

- Industry Analytics and Strategy

- Workforce Development

- Manufacturing

This article originally appeared in the December 2025 issue of Expansion Solutions magazine.

This article originally appeared in the December 2025 issue of Expansion Solutions magazine.

Advanced Manufacturing is outperforming traditional manufacturing on job growth and wages. While overall growth has moderated, Advanced Manufacturing continues to expand faster than traditional manufacturing and offers a significant wage premium—underscoring its role as a driver of high-value, technology-intensive employment.

Investment is shifting toward larger, capital-intensive, high-tech projects. Manufacturing investment increasingly favors Advanced Manufacturing subsectors such as semiconductors, clean energy, life sciences, and automation, with fewer but larger projects signaling long-term commitments to innovation-driven production.

Federal policy remains a powerful catalyst even amid uncertainty. Programs like the CHIPS and Science Act, Inflation Reduction Act, and infrastructure investments have reshaped where and how Advanced Manufacturing grows, particularly in EVs, batteries, and semiconductors. Policy shifts may affect pace, but not the sector’s strategic importance.

Talent constraints are the sector’s most pressing challenge. Employers face persistent shortages in STEM-heavy roles as traditional degree completions decline. At the same time, rising turnover and competition for skilled workers make workforce development a critical factor in sustaining growth.

Apprenticeships and employer-led training are essential to future competitiveness. Apprenticeships offer a proven pathway to build skills, raise earnings, and reduce turnover, especially as shorter, skills-based credentials grow. Communities that align employers, educators, and workforce systems will be best positioned to capture Advanced Manufacturing investment.

Over the past decade, Advanced Manufacturing has emerged as one of the most powerful engines of US economic growth. Fueled by federal investment, supply chain alignment, and rapid technological innovation, the sector is expanding faster than traditional manufacturing and creating new opportunities for communities across the country. From semiconductors to electric vehicles and precision medical devices, Advanced Manufacturing is not only generating high-quality jobs but also reshaping the skills and infrastructure required to remain competitive.

For economic developers, this transformation brings both promise and urgency. Capturing investment that is centered on Advanced Manufacturing activity requires a clear understanding of industry priorities and close relationships with the workforce and educational institutions that drive training initiatives. It also means engaging employers in shaping those training initiatives and strategically leveraging your community’s existing assets to access the maximum potential public sector support.

In this article, the definition of the Advanced Manufacturing sector is rooted in Camoin Associates’ industry experience. Our team recently completed projects in Maine, New Hampshire, and Missouri that aim to make the case for investment in various Advanced Manufacturing subindustries. To scale our industry definition nationally, we considered industries with an above-average share of STEM employment (approximately 12%) to reflect a combination of specialized skills, technological intensity, and innovation that characterize the sector.

The following sections examine recent industry performance in Advanced Manufacturing, the federal policies influencing expansion, the increasing importance of talent development, and the implications for communities positioning themselves to compete in this rapidly evolving landscape.

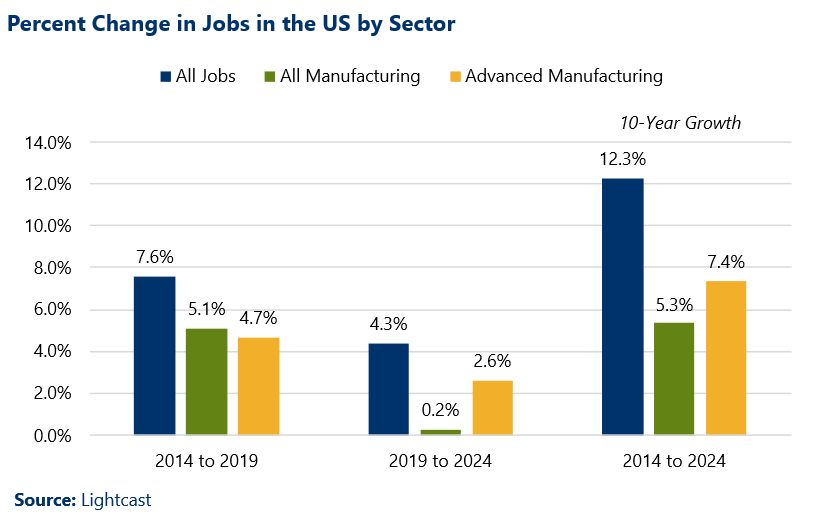

Over the past decade, Advanced Manufacturing has added more than 250,000 jobs in the US, growing 7.4%. Growth has slowed in the past five years (2019–2024), rising 2.6% compared with 4.7% between 2014 and 2019. Despite this deceleration, Advanced Manufacturing is still expanding nearly three times faster than overall Manufacturing, reflecting both a rising demand for products that rely on advanced technologies, such as electric vehicle components, semiconductors, and precision medical devices, and a broader industry shift toward manufacturing processes that use automation, robotics, and precision engineering to produce goods more efficiently.

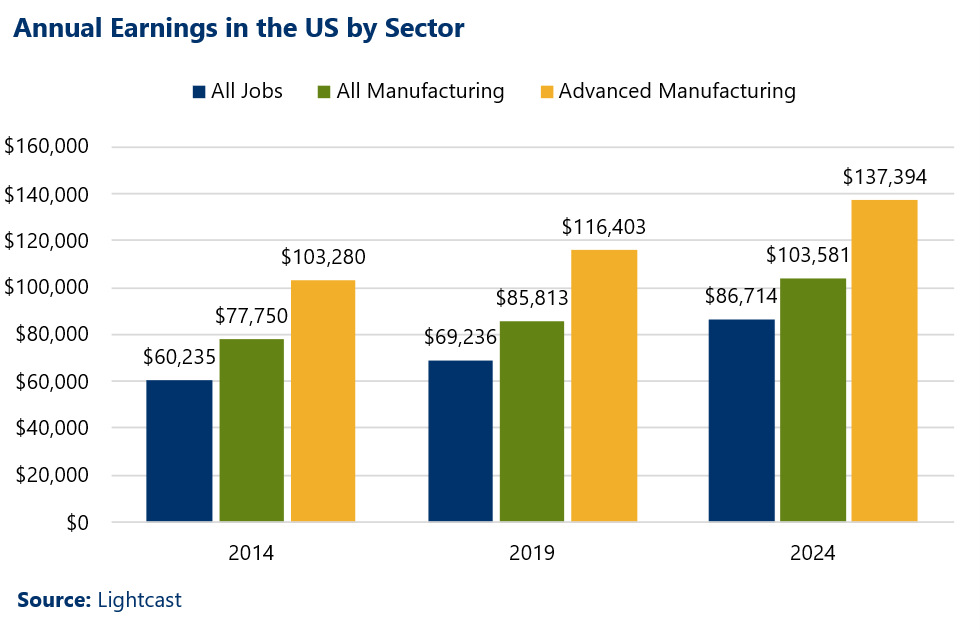

Despite slow wage growth in recent years (18% compared to 25% among all jobs and 21% among all Manufacturing jobs, not adjusted for inflation), earnings in the Advanced Manufacturing sector remain significantly higher than those of both the overall Manufacturing sector and the broader economy. In 2024, the average Advanced Manufacturing job paid nearly $137,400 (annually), compared with $103,600 across all Manufacturing jobs and $86,700 across all US jobs. This wage premium reflects the sector’s reliance on specialized skills and technical expertise. At this level, even modest wage growth signals continued demand for highly skilled labor and underscores the sector’s role in creating high-value employment opportunities.

Between 2019 and 2024, Advanced Manufacturing Gross Domestic Product (GDP) grew by 24%, compared with 31% across all Manufacturing and 36% for the US economy overall (Not adjusted for inflation; Source: Lightcast). While output growth has been more moderate, job growth in the sector still outpaced the broader manufacturing average, signaling expanding production activity.

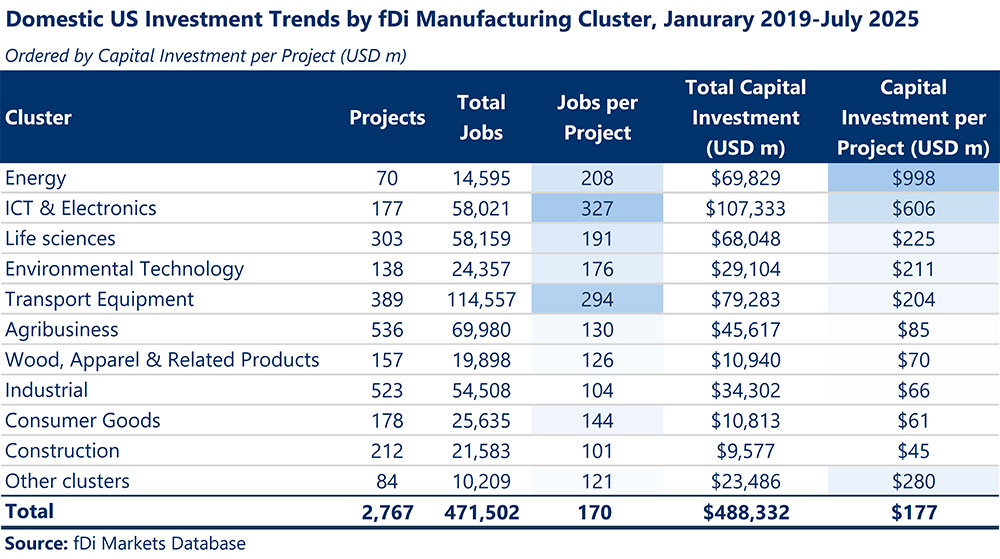

According to the fDi Markets Database, between 2019 and mid-2025, US domestic and international Manufacturing investment has led to nearly 5,300 projects, generating over one million jobs and nearly $1.1 trillion in capital investment. Domestic investment (meaning a company moving or expanding from one US location to another) alone generated more than 2,750 projects, over 471,000 jobs, and nearly $490 billion in capital investment.

Domestic investment activity peaked in 2021, reflecting post-pandemic supply chain reshoring and the early impact of federal manufacturing incentives. However, average project sizes have grown, with 2025 showing the highest average capital investment of nearly $250 million per project, signaling a shift toward larger, more capital-intensive facilities.

Capital-intensive projects are increasingly concentrated in Advanced Manufacturing industries such as automation, semiconductors, and clean-energy production. Although the fDi Markets Database reflects all Manufacturing activity, investment trends point toward Advanced Manufacturing dynamics. Clusters most closely associated with Advanced Manufacturing, such as Energy, ICT and Electronics, Life Sciences, and Environmental Technology, rank among the top generators of both capital investment and jobs per project. This suggests that Manufacturing investment is increasingly focused on high-tech, innovation-driven subsectors.

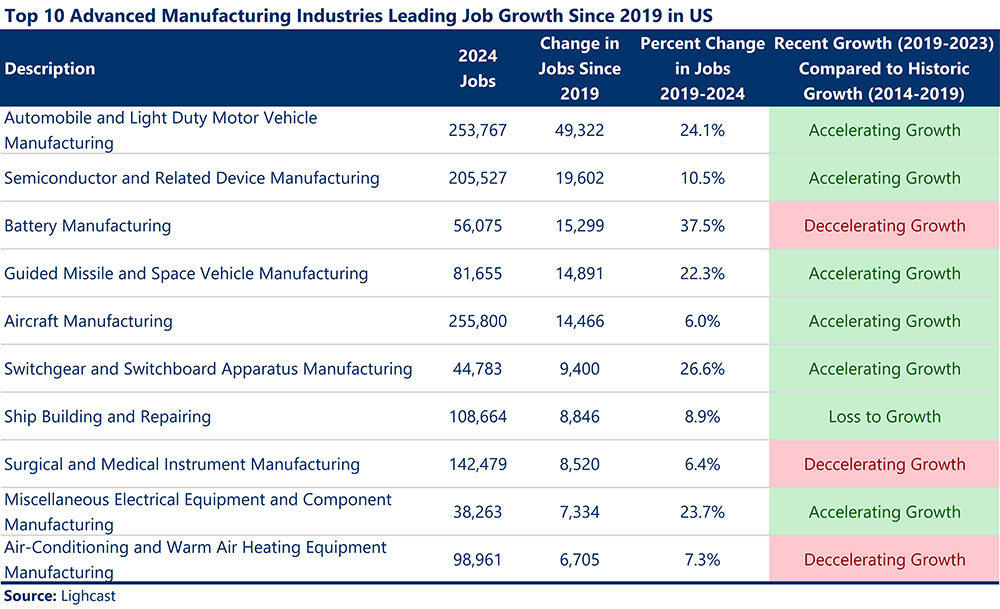

The sector’s job growth has been driven by the manufacturing of automobiles, semiconductors, batteries, aerospace products, and defense materials. These high-growth sub-industries indicate that the sector’s expansion is becoming increasingly tied to federal policies and related incentives, as well as the integration of robotics and digital systems into the production of goods.

Automobile and Light Duty Motor Vehicle Manufacturing led sector job growth in both 2014–2019 and 2019–2024. Over the past decade, technological advancements, most notably the rise of hybrid and electric vehicles (EVs), have fueled demand and reshaped the industry. According to the fDi Markets Database, US-based companies investing domestically between January 2019 and July 2025 saw substantial job creation, with Ford Motor Company, General Motors (GM), and Rivian Automotive generating 15,220, 12,519, and 10,066 jobs, respectively.

This growth has been driven by innovation, consumer demand, and federal policy. The Inflation Reduction Act (2022) offered up to $7,500 in tax credits for new EV purchases, provided $3 billion in loans for advanced vehicle and component manufacturing, and extended the Advanced Manufacturing production credit for clean energy technologies. Similarly, the Bipartisan Infrastructure Law (2021) allocated funding for EV-supportive infrastructure nationwide (Source: Electrification Coalition).

Other high-growth sectors, Battery Manufacturing; Switchgear and Switchboard Manufacturing; Miscellaneous Electrical Equipment and Component Manufacturing; and Air-Conditioning and Warm Air Heating Equipment Manufacturing, have similarly benefited from federal investment in the transition to clean energy.

While the One Big Beautiful Bill Act (2025) may moderate some EV and clean technology demand, the industry’s trajectory continues to be shaped by innovations in electrification, autonomous vehicles, and advanced safety standards, suggesting its role as a driver of Advanced Manufacturing will persist.

Separately, Semiconductor and Related Device Manufacturing has accelerated sharply in recent years, growing from 2.3% between 2014 and 2019 to 10.5% between 2019 and 2024. It is now the sector’s third-largest industry, with over 205,000 jobs as of 2024. The CHIPS and Science Act (2022) has committed $36 billion toward revitalizing the US semiconductor industry to strengthen economic and national security (Source: NIST.gov).

Key investments include Intel ($36.7 billion), Micron Technology ($22.2 billion), and Texas Instruments ($14.5 billion) since January 2019 (Source: fDi Data). The CHIPS Act specifically supported Micron’s expansion and modernization of its Manassas fabrication facility, onshoring technology previously produced in Taiwan. These investments enhance supply chain resiliency across automotive, industrial, and defense markets.

While changes in federal policy may create a more uncertain environment, especially for clean technology applications, core themes that can improve US competitiveness in Advanced Manufacturing remain embedded in various federal priorities. The Economic Development Administration (EDA), for example, continues to emphasize Manufacturing, Workforce, and Innovation and Entrepreneurship as three of its five investment priorities. The specialized nature of many Advanced Manufacturing roles, supported by ongoing upskilling and innovation from both the public and private sectors, presents numerous opportunities to strengthen domestic capabilities and reinforce the sector’s critical role in US economic and technological leadership.

Even as Advanced Manufacturing grows, employers report increasing difficulty recruiting, training, and retaining skilled workers. Across the sector, the turnover rate reached 27.5% in 2024 (Source: Lightcast), meaning employers had to replace nearly 28% of their workforce in addition to hiring workers to support industry growth. While this is lower than the 39% turnover rate across all Manufacturing jobs, likely reflecting higher pay in Advanced Manufacturing, employers still face challenges filling specialized STEM roles, which require skills that are in short supply.

As industry growth accelerates, hiring becomes more competitive within the industry, which can lead to labor shortages or make some manufacturers unable to compete. Developing a skilled workforce can help stabilize the industry and strengthen resilience against offshoring by reducing costs, accelerating innovation, and ensuring manufacturers can respond quickly to market shifts.

Among the 10 key growth industries within Advanced Manufacturing, the share of STEM workers ranges from 10% in Automobile Manufacturing to 31% in Semiconductor and Related Device Manufacturing. As manufacturers incorporate more advanced techniques into their processes and produce more technologically advanced products, the sector will increasingly rely on STEM workers.

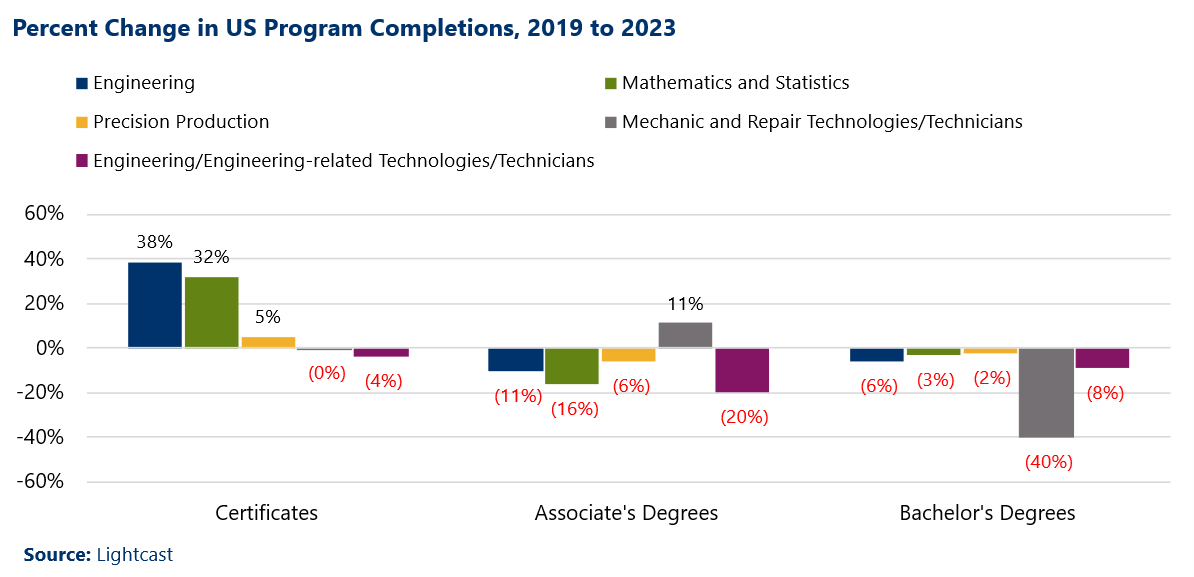

Between 2019 and 2023, completions in STEM-related programs critical to Advanced Manufacturing generally declined. Associate and Bachelor’s STEM programs saw fewer graduates, with the notable exception of Mechanic and Repair Technologies/Technicians associate programs, which increased by 11%. In contrast, certificate programs, particularly in Engineering and Mathematics and Statistics, experienced sharp growth in completions.

Fewer Associate and Bachelor graduates in STEM means the long-term supply of highly skilled workers is tightening, making it harder for employers to attract candidates for more technical, higher-skill roles. Meanwhile, the rise in certificate completions may reflect growing interest in shorter, skills-based training, which could help fill entry-level jobs. Employers may need to adapt hiring and training strategies to leverage these certificate earners effectively.

As traditional higher education pathways produce fewer graduates, Advanced Manufacturers can leverage apprenticeships to attract new talent, upskill certificate holders, and build a workforce pipeline through hands-on training that is unlike any classroom experience. Recognizing this potential, the federal administration has elevated apprenticeships as a key strategy to strengthen domestic manufacturing and boost productivity.

In April 2025, an Executive Order directed top officials to develop a plan to “reach and surpass 1 million new active apprentices” (Source: WhiteHouse.gov).

According to the US Department of Labor (DOL), which tracks registered apprenticeship programs, there are currently about 704,742 active apprentices across all 50 states, with additional programs in US territories. In FY 2024, more than 950,000 individuals participated in apprenticeship programs. Because five states do not consistently report to the federal system, the true number of active apprenticeships is likely higher than the published figures indicate. The DOL reports that Construction, Public Administration, and Educational Services are the top three industries with active apprenticeship programs, while Manufacturing ranks fifth on the list.

Reaching the administration’s goal of 1 million active apprenticeships will be a significant challenge. The Manufacturing Institute (MI), a nonprofit affiliate of the National Association of Manufacturers, developed a Workforce Blueprint to guide the effort. MI emphasizes that while apprenticeships are a proven model, they need stronger support to scale effectively. Employers must be at the table shaping federal policies and programs to ensure alignment with industry’s evolving needs. Just as important, stable and predictable funding is essential so businesses can plan training investments with confidence (Source: The Manufacturing Institute).

Apprenticeships not only meet employer needs but also create transformative opportunities for workers. At the Manufacturing Association of Central New York (MACNY), which serves more than 300 businesses and organizations, apprenticeship and pre-apprenticeship programs support individuals ranging in age from 18 to 71. These programs engage both employed and unemployed participants, providing multiple on-ramps into Advanced Manufacturing careers and reinforcing the long-term value of apprenticeship models.

The Kansas Department of Commerce reports that the average starting salary of someone who completes an apprenticeship program is $80,000. Beyond just starting wages, researchers at the Urban Institute found that earnings for participants in DOL-registered apprenticeship programs increased by 49% following completion, outpacing the 16% growth experienced by comparable workers who did not participate (Source: Gardiner, 2023). This reflects the value of specialized skills and on-the-job experience. With the benefit of competitive wages, apprenticeships not only attract new talent to Advanced Manufacturing but can also help retain skilled workers and reduce turnover, overall reducing strain on the employer.

With evolving workforce needs, changing federal policies, and a hyper-competitive investment environment for businesses that can offer quality, high-wage jobs to residents, economic developers have to manage how resources are deployed to best position their community. Based on the current market and where Advanced Manufacturing is expected to trend in the short to mid-term, here are three things that economic development teams can prioritize now.

If Advanced Manufacturing is a target industry or emerging opportunity in your community, employers must be active participants in workforce conversations through advisory boards or other industry work groups. Engaging a cross-section of manufacturers helps identify both shared training needs and specialized skill gaps. In rural areas, where achieving scale can be difficult, aggregating demand across employers and emphasizing transferable skills can make training programs more achievable. While collaboration between economic development and workforce systems is improving, continued integration is critical to ensuring these conversations drive meaningful outcomes.

Stay informed about policy directions and funding streams tied to Advanced Manufacturing. Accessing these resources can help communities align local strategies with national initiatives and unlock new investments. While it is not advisable to constantly chase shifting federal or state priorities, communities should assess where they are well-positioned to benefit from current funding emphasis. For example, if apprenticeship expansion or workforce training capacity has long been a local priority, now may be the time to partner with workforce boards to align for potential funding opportunities.

Maintain an up-to-date inventory of industrial and commercial sites to support Advanced Manufacturing growth and related supply chain activity. Communities located near recent investments, like those around Manassas, VA, or Syracuse, NY, are especially well-positioned to capture spillover opportunities. Understanding how local assets fit into the broader supply chain ecosystem can make the difference between seizing an opportunity and missing investment potential for your community. This preparation must also include conversations and close relationships with planners and local planning boards to verify that potential Advanced Manufacturing activities are allowable in desirable locations.

Alexandra Tranmer, CEcD, is the Director of Industry and Workforce at Camoin Associates. She has an Honors Bachelor of Arts degree and a Master of Science degree in Planning (MScPl) from the University of Toronto in Ontario, Canada. As a senior project manager, Alex has led complex strategic planning efforts in geographies ranging from bustling urban centers to pastoral tourist destinations, requiring adept stakeholder management and collaboration. She works with clients to balance the competing interests of stakeholders while ultimately helping them develop an ambitious yet achievable plan under their current organizational climate.

Bailey McConnell is a Senior Economic Data and Research Analyst at Camoin Associates. She holds a Master of Interdisciplinary Studies, Urban Studies, degree from Georgia State University and a Bachelor of Arts degree in Economics from Boston University. Bailey’s professional background spans economic development, public policy, and real estate advisory. She has contributed to business attraction efforts in Georgia and completed industry and workforce analysis, real estate and market analysis, and housing analysis projects for clients across the country for Camoin Associates. Bailey is passionate about storytelling with data and helping communities generate equitable economic prosperity.

Learn about our industry analytics and strategy services

Learn about our workforce development and talent retention services

Real Estate Development and Housing

Ready to move your community forward? Discover how tailored market analysis and strategic public investments can unlock new development.

Industry Analytics and Strategy

Industry Analytics and Strategy

Your resource for understanding today and looking toward tomorrow