- Navigator

- Aerospace

- Expansion Solutions

- Industry Analytics and Strategy

This article originally appeared in the March/April 2024 issue of Expansion Solutions Magazine.

This article originally appeared in the March/April 2024 issue of Expansion Solutions Magazine.

The Aerospace and Defense industry has been getting a lot of attention in the news recently. Top stories include exciting innovations in autonomous technology, space exploration, defense needs related to new and continuing global conflicts, and clean technology including advances in power sources and fuels. There has also been coverage of topics of concern within the industry, including recent high-profile equipment malfunctions and security failures.

This attention will likely continue as Aerospace and Defense is a critical industry not only for our economy but also for national security, business and leisure travel, space exploration and development, and our continued advancement of new technologies serving multiple industry sectors.

Aerospace and Defense is comprised of many core industries within aircraft manufacturing, including guided missiles, space vehicles, explosives, ammunition, and arms, military vehicles, and all their related parts and systems. There are also a number of related industries within the supply chain such as metals, plastics, composites, electronics, information technology, and professional and technical services including engineering and R&D.

In this article, we will focus on a core subset of industries considered part of or connected to Aerospace and Defense, their economic performance, and what is driving economic opportunities and investment. The supply chain for Aerospace and Defense is expansive and therefore creates multiple opportunities across many sectors and subsectors. A detailed listing of the specific industries and the associated North American Industry Classification Codes (NAICS) is included at the end of this article.

The Aerospace Industries Association has represented the industry since 1919. It provides an annual economic assessment of the industry[1] which highlights the significant positive contributions year after year, including:

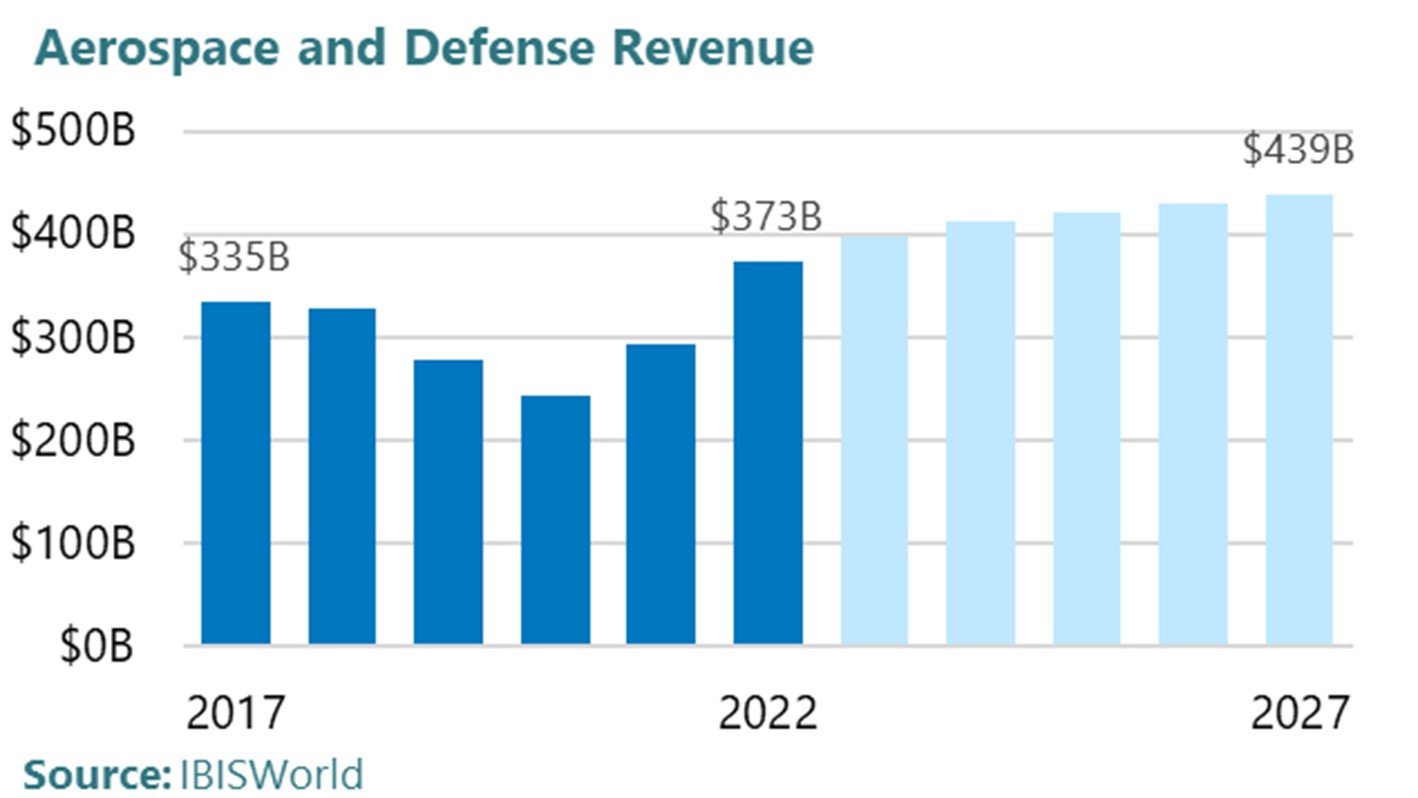

Digging deeper into recent data from multiple sources supports this assessment of the industry. In 2022, Aerospace and Defense revenues were estimated at $373 billion in the US, a substantial increase over the 2017 level of $335 billion and an indication of recovery from the declines experienced in 2019 and 2020 driven by COVID-19 and supply chain constraints.

IBISWorld projects this revenue turnaround will continue and estimates that Aerospace and Defense revenues will reach $439 billion by 2027. Within the industry group, Aircraft, Engine, and Parts Manufacturing represent by far the largest source of revenues, an estimated $300 billion in 2022.

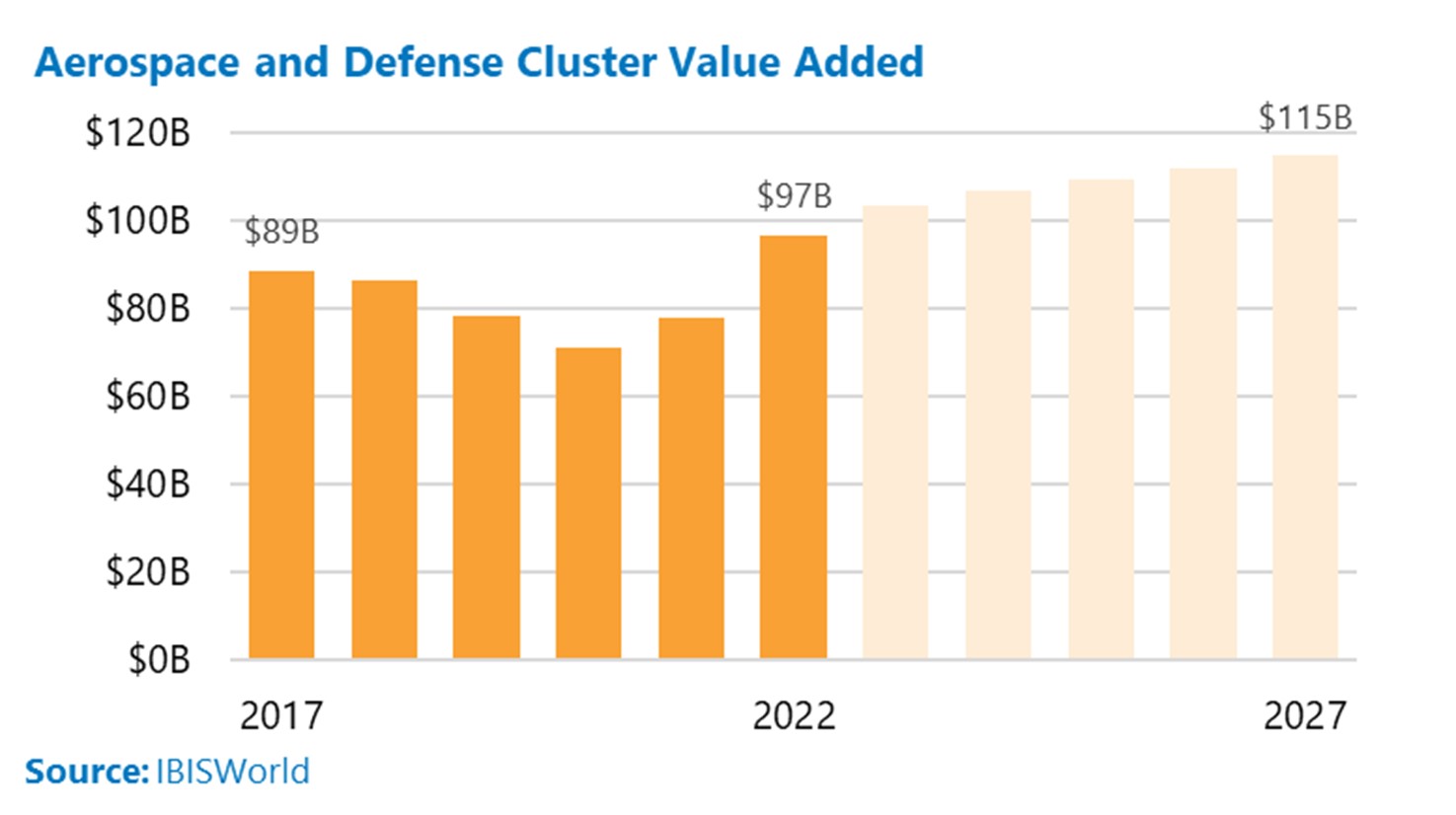

Supporting strong output and economic benefit, Aerospace and Defense is a “high-value” industry, meaning its revenues are significantly higher than the cost of the goods and services it uses in production. Aerospace and Defense’s value[2] add in 2022 was estimated at $97 billion and is projected to reach $115 billion by 2027.

In terms of employment, Aerospace and Defense had an estimated 574,271 jobs in 2002 with 71% specifically related to aircraft and related parts. Another 17% of jobs are within Guided Missile and Space Manufacturing and related parts.

Earnings and related wages per job are relatively high in Aerospace and Defense, averaging $135,222/year in 2022.

The top occupations in Aerospace and Defense are a mix of production (CNC and other machining, tooling, and metal working), engineers, computer software, and supervisors and managers requiring either degrees or moderate on the job training.

Increasingly, industry employers report needing more employees with skills in IT, problem-solving, communications, the ability to work in teams, and the ability to work with integrated technology including robotics.

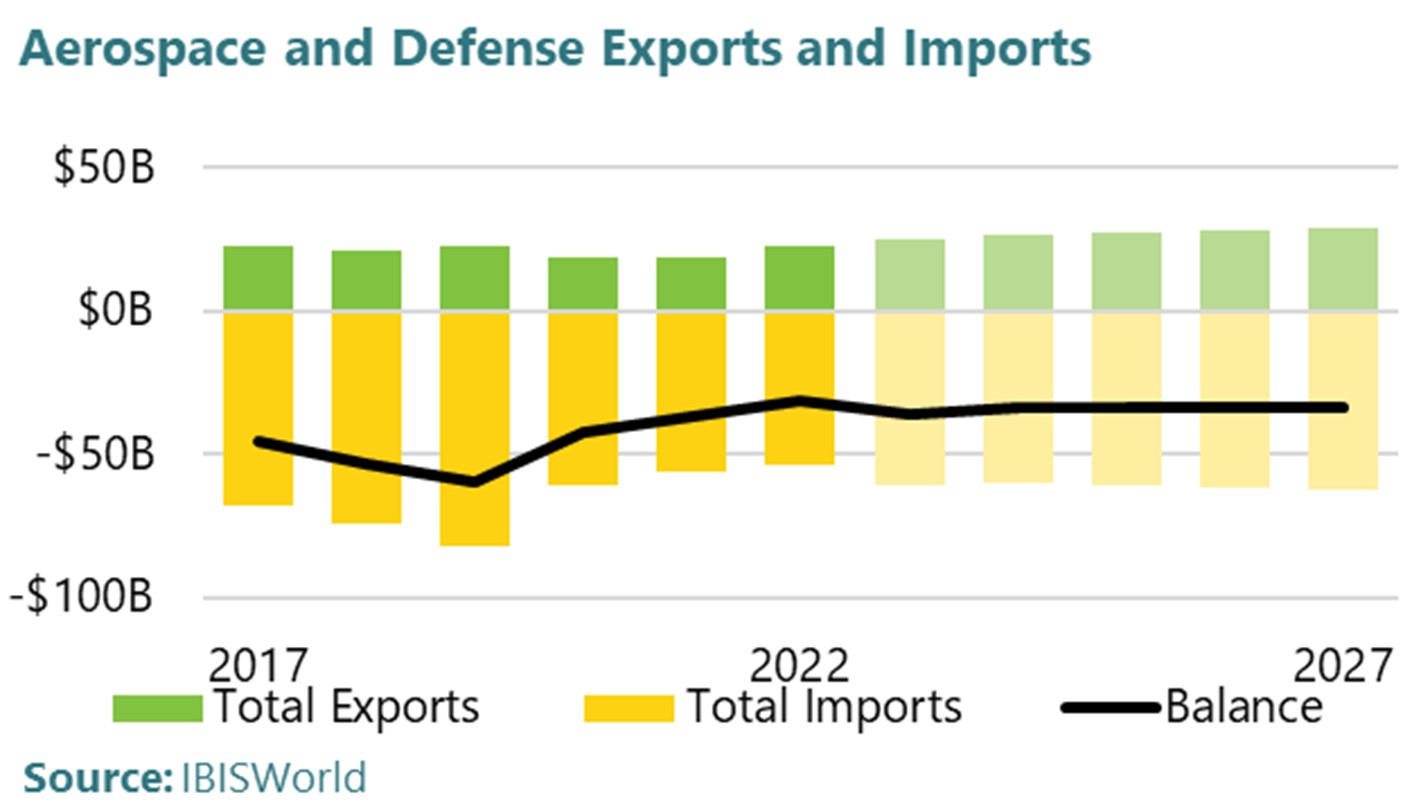

Aerospace and Defense is both a high exporter and importer of goods and services. According to IBISWorld, exports in 2022 totaled approximately $23 billion, representing 6% of revenues for all industries in the US. That same year imports totaled approximately $54 billion, resulting in a trade deficit of $31 billion. Federal efforts to produce more goods and services in the US and through onshoring efforts will help stabilize this trade deficit, however imports will likely remain high to meet industry needs within global supply chains and markets. It is worth noting that non-defense activity in Aerospace is typically high in exports and contributes positively to the US trade balance.

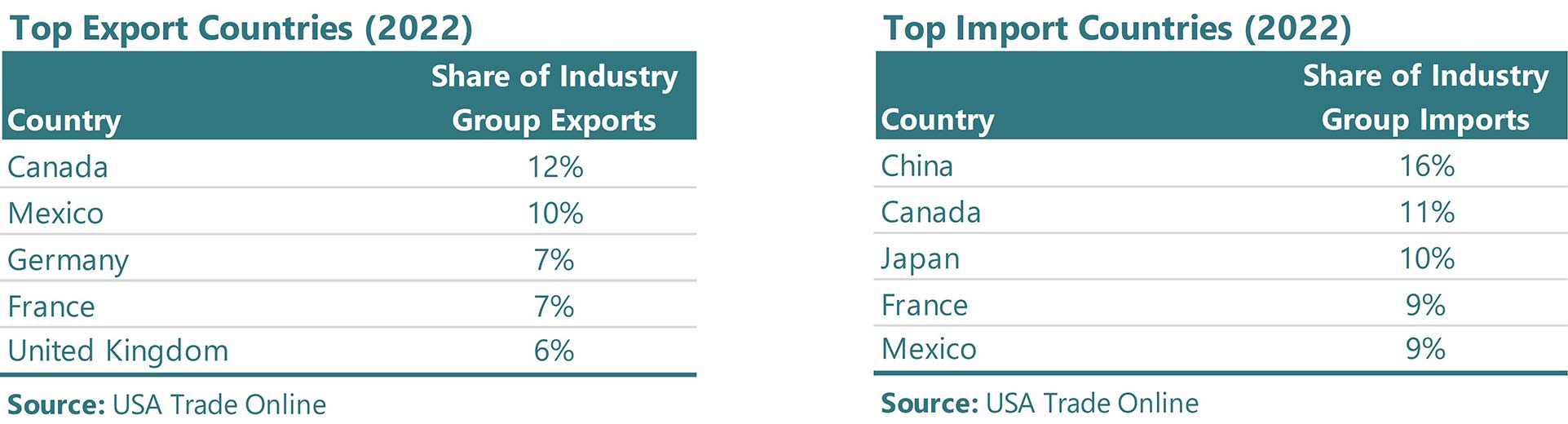

Canada and Mexico are the largest recipients of Aerospace and Defense exports, each accounting for 10% or more of the industry group’s 2022 exports. China and Canada are the main sources of the industry group’s imports, supplying 16% and 11%, respectively, of total imports.

Raytheon Technologies is the largest Aerospace and Defense company in the US, with a market share of 10.3% in 2022. The next largest by market share are Boeing Company and GE Aviation UK, with 8.4% and 5.5%. Other significant players include Lockheed Martin Corporation (4.7%) and General Dynamics Corporation (1.3%).

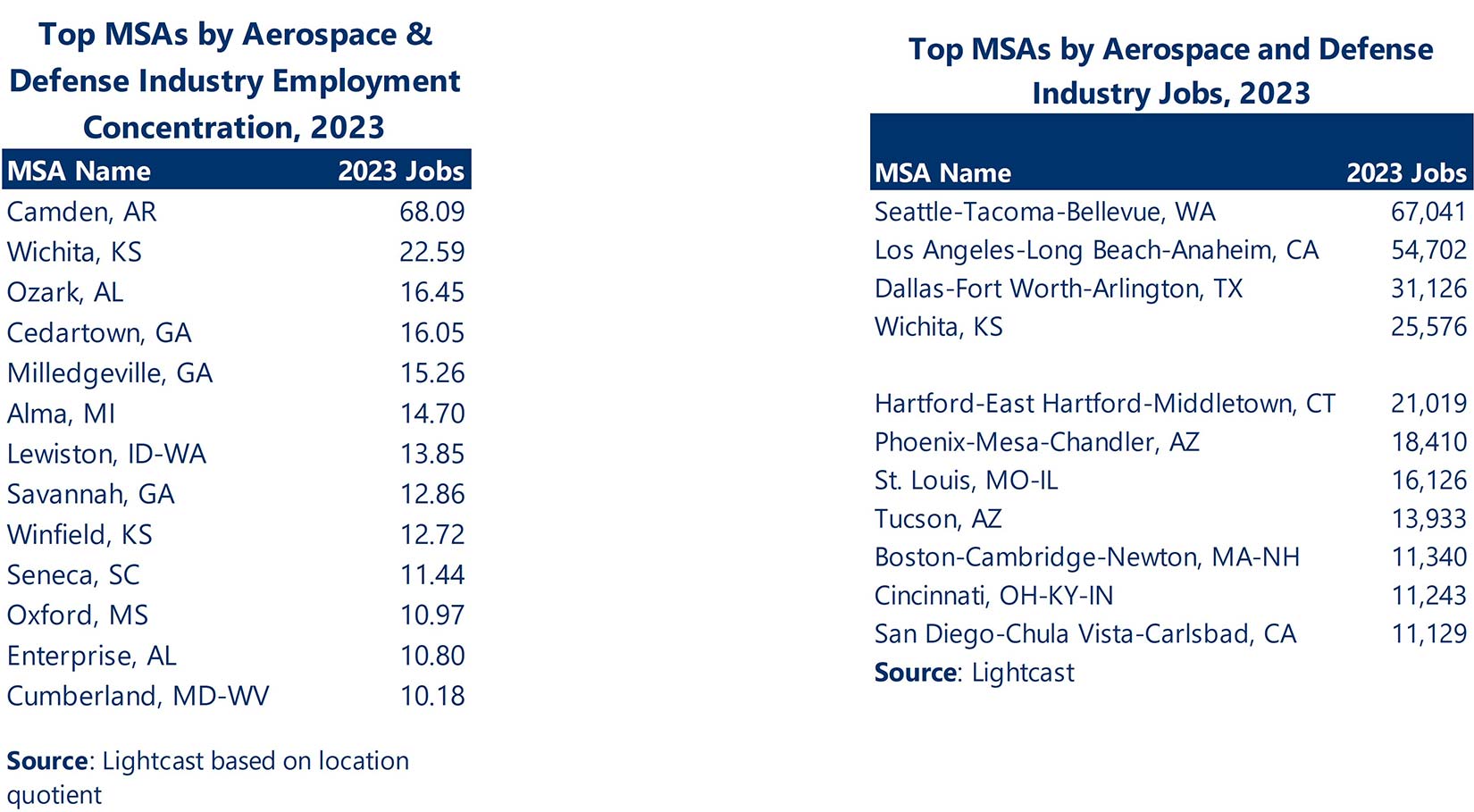

Data on total jobs and job concentration reveal Aerospace and Defense hubs in major metropolitan areas, many of which feature significant airport facilities or proximity to multiple facilities. This includes Seattle, WA, Los Angeles, CA, Dallas, TX, and Hartford, CT.

Smaller metropolitan areas can have a larger job concentration relative to total jobs in all sections, and the most concentrated include Camden, AK, Wichita, KS, Ozark, AL, Cedartown, GA, and Milledgeville, GA.

There are numerous factors that impact and drive economic development trends and opportunities in Aerospace and Defense. The following is an overview of the more critical factors related to recent and emerging activities.

Innovation and entrepreneurship are driving growth in existing and emerging regional hubs. This includes growth of test sites, R&D, technology, and commercialization.

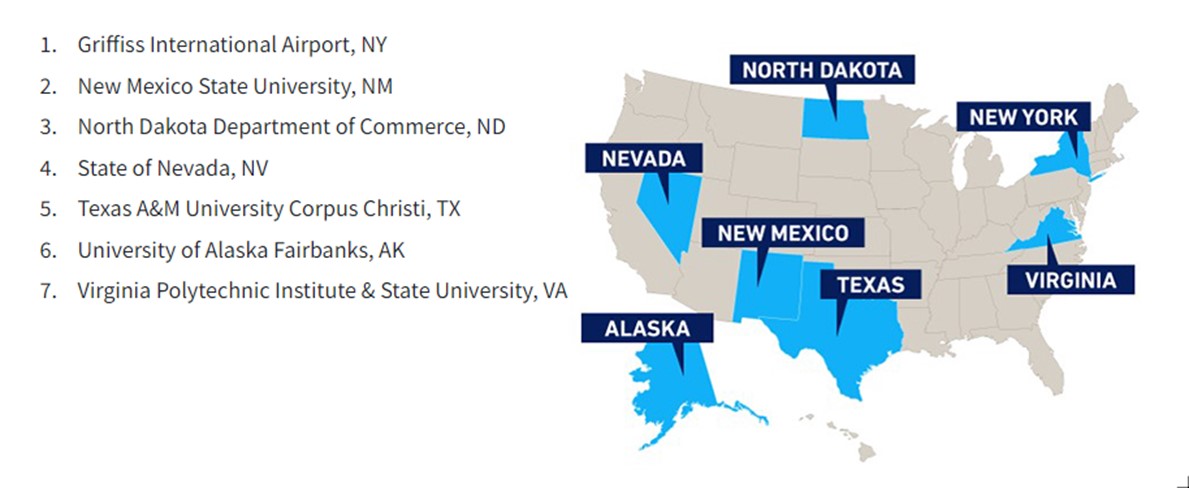

Test sites for Unmanned Aircraft Systems (UAS) are seeing significant growth and investment. The Federal Aviation Administration (FAA) has seven UAS test sites across the country that are generating emerging industry activity.

In addition to the FAA test site locations, innovation related to Aerospace and UAS is also emerging in other regions.

GENIUS NY is a startup accelerator in Syracuse sponsored by Empire State Development, which invests $3 million annually into seed-stage startups focused on uncrewed aerial systems, automation, and artificial intelligence (AI)[3]. It is located near Griffiss International Airport at the Griffiss Business Technology Park in Rome, NY, and is operated by Oneida County. This is creating a targeted growth corridor from Rome to Syracuse.

Detroit’s Advanced Aerial Innovation Region is a recent entrant into UAS and drone hub development. A partnership between Ford affiliate Michigan Central and the Michigan Department of Transportation, it is the first cross-sector, advanced aerial urban initiative in the US. It seeks to attract drone company startups, provide high-skill job training, and advance public policy related to the commercialization of drone technology in the state[4].

The AeroPark Innovation District located at and adjacent to St Mary’s County Airport in Maryland is also a recent entrant hoping to create a hub of Aerospace and Defense activity. It encompasses the University of Maryland UAS Test Site; TechPort business accelerator; aviation and aeronautic companies including PaxAero, Solutions, ABSI Aerospace & Defense, MTECH, and AIRtec; and the Wildewood Professional and Technology Park and retail areas.

The Tulsa Hub for Equitable & Trustworthy Autonomy (THETA) in Oklahoma was recently designated as one of 31 Tech Hubs to receive federal funding from the US Department of Commerce’s Economic Development Administration. THETA will focus on unmanned aerial systems, drones, cybersecurity, and generative artificial intelligence and is an excellent example of the importance of regional collaboration for success in Aerospace and Defense. Led by Tulsa Innovation Labs, the partnership includes Tulsa Regional Chamber of Commerce, University of Oklahoma, Oklahoma State University, Tulsa Community College, Oklahoma Aeronautics Commission, and many more.

The Los Angeles region has long been an area dense with Aerospace activity and is seeing considerable investment as a hub for emerging technologies and commercialization. Among the coordinating partners from an economic development perspective is the SoCal Aerospace Council.

The council’s purpose is to build and sustain the most globally competitive Aerospace and Defense cluster. This effort is building on and succeeding in growth with involvement from multiple top companies, including Relativity Space, SpaceX, Rocket Lab, and many more.

In almost all cases, innovation advances in Aerospace and Defense are being led by or are occurring parallel to advances in information and digital technologies. Examples include:

This increased use of data and information technologies within Aerospace and Defense is also simultaneously increasing the necessity and demand for enhanced cybersecurity.

Another major area of innovation and technology is cleantech, which uses technology to reduce carbon emissions and depletion of natural resources, increase the use of renewable energy and materials, and help companies improve efficiency by requiring less energy or materials. For Aerospace and Defense, this includes integration of cleaner fuels (biofuels), advanced materials (lighter stronger, sources from cleaner raw materials such as bioplastics), electrification, R&D, and commercialization of hydrogen technologies.

Cleantech is being integrated within the Aerospace and Defense industry in response to global consumer trends and demand, which are driving new regulations, policies, and incentives, and as a way to reduce costs and improve performance. According to IBISWorld, “Concerns about sustainability and the industry’s reliance on fossil fuels have driven demand for electricity-based solutions to air travel that are more environmentally friendly. Viable electric models have already gone airborne with the help of lightweight body and engine compositions, though some look to hydrogen planes as a more practical solution. While electric cars are a modern reality, battery limitations and a lack of regulatory frameworks have dramatically slowed the technology’s adoption in air travel. To address this, manufacturers will continue partnering with electric vehicle companies and invest heavily in exploring electric propulsion technology.”

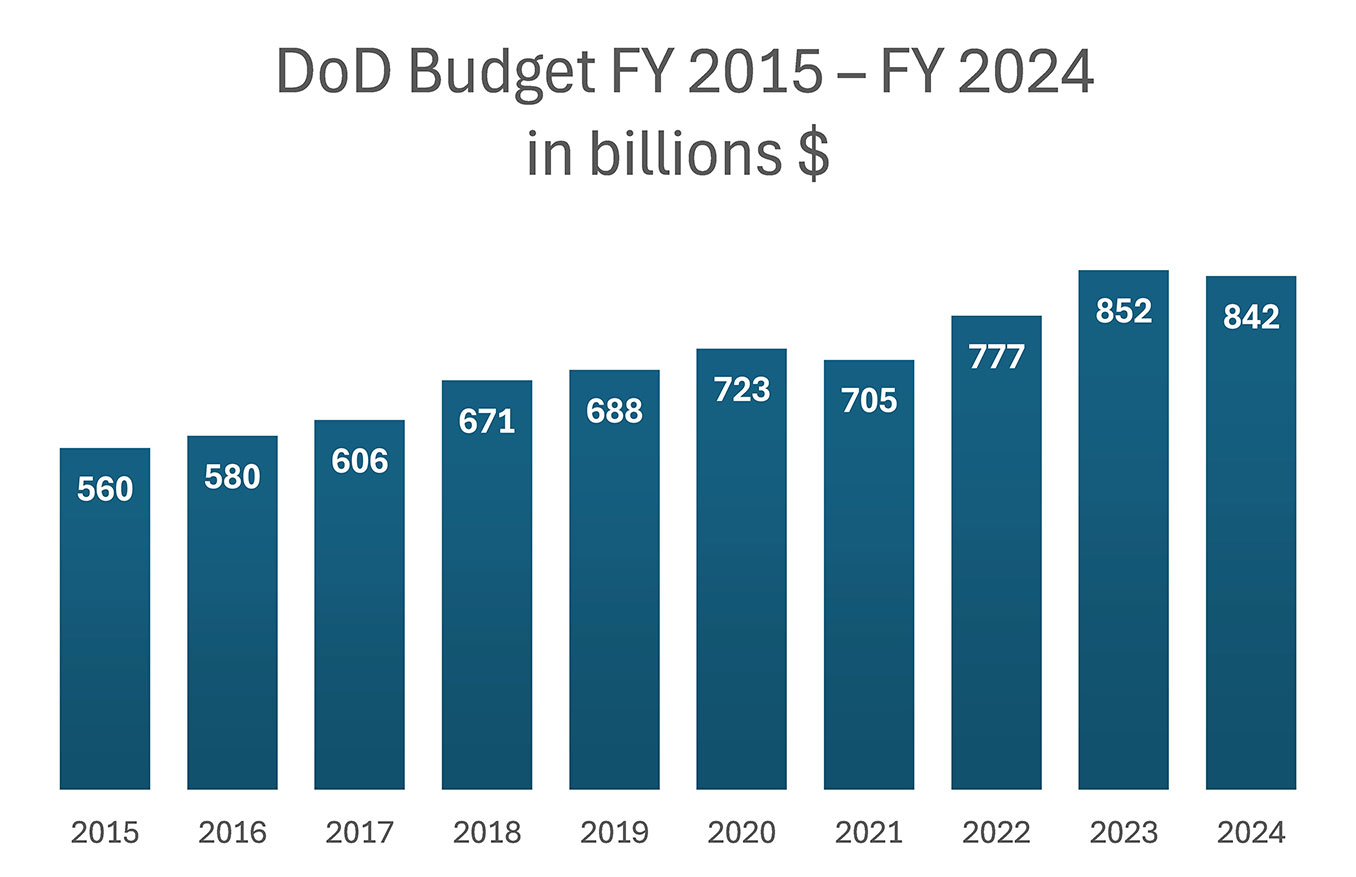

Federal spending by the US Department of Defense (DOD) plays a significant role in the demand for the Aerospace and Defense products and services. In the past ten years, DOD budgets have grown substantially, increasing from $560 billion in 2015 to $842 billion in 2024.

Source and Notes: Defense Budget Overview, United States Department of Defense, Fiscal Year 2024 Budget Request; Includes Global War on Terror/Overseas Contingency Operations and other supplemental funding including funding for Ukraine.

This increase in US defense spending is consistent with global trends. According to ResearchAndMarkets.com, which released a 2023 report on the global Aerospace and Defense market, “The defense industrial base across US [and] Europe is gearing up to ramp-up production rates over near term to refill depleting stockpiles of munitions, missiles, [and] weapons following the rapid rate at which they are being used in Ukraine and to meet growing international orders. The global defense spending, thus, is projected to reach the record $2.5 trillion level by 2027 as the industry prepares to ramp up production rates to unprecedented rates [and] level over near to medium term to meet huge global demand, replenish depleted inventory levels and develop next generation capabilities with significant investments underway towards R&D as well.”

In addition to DOD spending, US government spending has long played a role in the trajectory of the Aerospace and Defense sector. In addition to the typical annual budget allocations, this has been especially true in the last three years, as there have been numerous blockbuster government spending bills aimed at transforming the nation’s infrastructure, energy, and manufacturing sectors.

Three pieces of legislation that will have a notable impact on Aerospace and Defense industries include the Infrastructure Investment and Jobs Act (passed in November 2021), the CHIPS and Science Act (passed in August 2022), and the Inflation Reduction Act (passed in August 2022). Much of the federal investment is driven by the desire to ramp up manufacturing within the US, to accelerate the application of AI and other digitals technologies, and to fast track the research and application of sustainable fuels and practices that will make the industry more resilient and lessen its impact on the environment.

The federal government set a goal to reach net-zero greenhouse gas emissions in the US aviation sector by 2050[5] and pieces of the Inflation Reduction Act seek to incentivize this transition and mitigate industry’s impact on climate change. This includes grants that encourage the use of sustainable aviation fuels (SAF) and low-emission technology.

The Fueling Aviation’s Sustainable Transition (FAST) grant program will award a total of $244.5 million to a range of users in the industry. Private sector companies can apply for the funds, along with other stakeholders like airports, air carriers, universities, local governments, and nonprofits.[6] The latest round of applications is currently being reviewed and additional funding is set aside in the coming years.

The Infrastructure Investment and jobs Act (IIJA) stands as one of the nation’s largest investments in infrastructure. It includes $25 billion in funding for aviation-related items like airports and air traffic control. These investments are severely overdue according to the American Society of Civil Engineers (ASCE), an industry group that gave US aviation infrastructure a D+ rating in their 2021 Report Card for America’s Infrastructure.[7]

The objective of the CHIPS and Science Act is to incentivize the production and innovation of semiconductor chips across the US. These chips are prevalent in the aerospace industry and the availability to secure them is critical to the stability of both the commercial and defense side of the industry. The CHIPS Program Office notes that while there is no fixed amount for awards, they anticipate their investments to range between 5-15% of the applicant project’s total capital expenses. The first Notice of Funding Opportunity was released in February 2023 and there were several waves of funding for different parts of the industry.

Applicants are asked to demonstrate their level of commitment to the project, which is judged based on the level of coordination with other local and state incentives, the amount of private capital leveraged compared to the grant ask, and the status of site evaluation if the project is construction focused.[8]

Additional funding opportunities will be available in the coming years around the production, construction, workforce, and research and development.

At the end of 2023, the federal government awarded the very first CHIPS and Science Act grant to BAE Systems, based in New Hampshire. The Aerospace and Defense government contractor received a $35 million grant to quadruple its semiconductor production capabilities. The US Commerce Department says that it expects to roll out around $53 billion in CHIPS and Science Act grants.[9]

Commercial aircraft, engines, and parts are a major part of all Aerospace and Defense activity. They are primarily driven by consumer demand which can be measured by enplanements. Impacted significantly by COVID-19, air travel has since rebounded. According to the US Department of Transportation, Bureau of Transportation Statistics, based on October seasonally adjusted data:

On recent and future demand, IBISWorld reported in 2023: “Despite a collapse of demand for air travel and new airplanes amid the COVID-19 pandemic, the pent-up demand in its aftermath brought a surge of air transit that boosted revenue as airlines sought replacements for planes and plane parts.”[10]

However, IBISWorld also indicated this demand was somewhat muted: “Climbing inflation has led to plummeting consumer confidence, discouraging travel. This trend has rippled through consumer aerospace markets, counteracting post-pandemic growth.”[11]

Consumer sentiment has also been impacted by safety concerns and service disruptions that have gained significant media attention. According to IBISWorld: “Commercial air transit represents the largest revenue stream, so steadily improving consumer sentiment will drive growth. Domestic and international trips by US residents will reliably and notably climb over the next five years, representing a continued interest in travel following the still-lingering pandemic lockdowns.”[12]

In addition to negatively impacting air travel, COVID-19 also directly impacted Aerospace and Defense supply chains. The impact was significant, and the recovery was slow. Supply chains have also been impacted by the reduced availability of computer chips and critical minerals and continued threats and disruptions from global conflicts. Additional computer chip capacity is being added within the US through the federal funding programs mentioned earlier in this article but is not yet online.

In addition to building physical capacity, technology is increasingly being deployed to make supply chains more efficient, responsive, and resilient. According to an article published by Deloitte Research Center for Energy & Industrials: “The A&D supply chain is a complex, globalized ecosystem of customers and original equipment manufacturers; multiple tiers of suppliers; and maintenance, repair, and overhaul providers. This complexity makes implementing diversification and transparency across the value chain extremely difficult, but imperative.[13]”

This is where technology is increasingly coming into play. The Internet of Things (IOT), as well as sensors, blockchain, and AI are all being piloted and integrated into supply chain applications. Adaptive manufacturing (3D Printing) also provides the ability to some make parts and materials on site, reducing the need for warehousing and transporting.

According to an article on Aerospace and Defense technology trends published recently by Epicflow: “The main advantage of additive manufacturing for the aerospace sector is that it improves manufacturing efficiency (thanks to rapid prototype development) and makes it possible to produce more lightweight components for aircraft, spacecraft, and satellites. This is especially relevant in the context of post-pandemic production ramp-ups in the aerospace realm; the technology makes it possible to reduce production costs, optimize fuel consumption, and generally gives aerospace manufacturers a competitive advantage.”[14]

Aerospace and Defense industry employers require a workforce with traditional advanced manufacturing skills in production, engineering, and related field, but are increasingly seeking workers with IT/digital skills. Furthermore, due to rapid changes in technology, no one can be expected to learn and be skilled at both what is needed and applicable in today’s industry as well as what might be required five years into the future and beyond without the strong commitment of industry, companies, and the education and workforce system for providing workers with continuous and adaptive learning.

This is all occurring in the midst of workforce shortages and competition for workers across all industries which is unlikely to subside in the mid-to long term future given the retiring population and demographics of the population in the US.

Companies and industries will need to significantly increase opportunities for training and education through partnerships with government and academia. This will need to be coupled with increasing the flexibility of traditional shiftwork, compensation and benefit increases, and providing a supportive work environment that meets workers needs within the region and localities where work is done in the form of housing, family care, and transportation.

The economic trends and opportunities presented in this article affect Aerospace and Defense companies all the way from start-ups to large global companies. Economic and business developers seeking to support these companies or attract new companies and investment will benefit from a focus on strategies and actions within three key areas.

Support Workforce Development: While support to retain and attract workers exists across numerous occupations and skill areas the most critical for Aerospace and Defense are those within manufacturing and production, engineering, and information technology. Successful workforce development efforts will require close collaboration between industry, education, and workforce partners. The focus should be on providing continuous training and the modernization of skills to include critical thinking, problem solving, and communications alongside technology. Supporting and partnering with high school career and technical centers as well as community colleges can have the most immediate impact.

Focus Marketing Efforts on Attraction and Investment: Aerospace and Defense require specific methods and data for marketing and business attraction. It is important to understand foreign and domestic trade and supply chains to be able to align with your niche and assets, including R&D, workforce, and location.

Specific Aerospace and Defense trade shows and conferences to consider attending for business and economic development include:

Foster Regional and Cross-Sector Partnerships: The footprint of Aerospace and Defense industry typically spans multiple states or regions and involves a variety of sectors within the value and supply chains. No one region can compete alone and no one organization can provide all the effort and services needed to succeed. Help develop and sustain collaborative relationships with the organizations, companies, schools, and agencies in your community.

📍 Related Article: The Space Economy: Legacy Industries and Emerging Trends

Learn more about Camoin Associates’ Industry Analytics and STRATEGY services

[1] “Supporting the Economy: At-a-Glance,” Aerospace Industries Association, https://www.aia-aerospace.org/industry-impact/#supporting-the-economy.

[2] Industry Value Added (IVA): The market value of goods and services produced by the industry minus the cost of goods and services used in production. IVA is also described as the industry’s contribution to GDP, or profit plus wages and depreciation.

[3] “About GENIUS NY,” GENIUS NY website, https://geniusny.com/about/.

[4] “Michigan Central, MDOT Launch Advanced Aerial Innovation Region in Detroit to Accelerate Commercial Drone Development” news release, Michigan Department of Transportation, October 25, 2023, https://www.michigan.gov/mdot/news-outreach/pressreleases/2023/10/25/mi-central-mdot-launch-advanced-aerial-innovation-region-in-det-to-accelerate-commercial-drone-dev.

[5] “US Sets Goal of Net-Zero Aviation Emission by 2050,” Reuters, November 9, 2021, https://www.reuters.com/business/cop/us-sets-goal-net-zero-aviation-emissions-by-2050-2021-11-09/.

[6] “Fueling Aviation’s Sustainable Transition (FAST) Grants,” Federal Aviation Administration online, December 4, 2023, https://www.faa.gov/general/fueling-aviations-sustainable-transition-fast-grants.

[7] “2021 Report Card for America’s Infrastructure: Aviation,” American Society of Civil Engineers, https://infrastructurereportcard.org/cat-item/aviation-infrastructure/.

[8] “Your Guide to the CHIPS Act Application,” BDO USA, April 12, 2023, https://www.bdo.com/insights/industries/manufacturing/your-guide-to-the-chips-act-application.

[9] “Biden-Harris Administration and BAE Systems, Inc., Announce CHIPS Preliminary Terms to Support Critical US National Security Project in Nashua, New Hampshire,” US Department of Commerce press release, December 11, 2023, https://www.commerce.gov/news/press-releases/2023/12/biden-harris-administration-and-bae-systems-inc-announce-chips.

[10] “Aircraft, Engine & Parts Manufacturing in the US – Market Size, Industry Analysis, Trends and Forecasts (2025-2029)”, IBISWorld, November 2023, https://www.ibisworld.com/united-states/market-research-reports/aircraft-engine-parts-manufacturing-industry/.

[11] Ibid.

[12] Ibid.

[13] Lindsey Berckman, Tarun Dronamraju, Kate Hardin, and Matt Sloane, “2024 Aerospace and Defense Industry Outlook,” Deloitte Research Center for Energy & Industrials,

[14] Victoria Sokolova, “Driving Digital Transformation in Aerospace & Defense: Technology Trends in 2024,” Epicflow, January 3, 2024, https://www.epicflow.com/blog/driving-digital-transformation-in-aerospace-defense-recent-technology-trends/.

Economic and Fiscal Impact Analysis

A recent analysis of a digital equity program in Westchester County, NY, revealed that it generated outsized economic benefits and return on investment for the community.

Business Retention and Expansion (BRE)

Industry Analytics and Strategy

Your resource for understanding today and looking toward tomorrow