- Navigator

- Food and Beverage

- Manufacturing

- Expansion Solutions

- Industry Analytics and Strategy

This article originally appeared in the June 2024 issue of Expansion Solutions Magazine.

This article originally appeared in the June 2024 issue of Expansion Solutions Magazine.

The Food Manufacturing sector has seen steady growth over the past five years, particularly in animal processing and bakeries. However, when looking at the food industry as a whole, traditional industry data sources (NAICS) overlook food categories and emerging trends. Alternative proteins and plant-based foods are one example of this.

In this article, we take a deeper dive into the growing $8 billion alternative proteins and plant-based foods industry, which has been on a sharp upward trajectory in recent years, with growing market penetration when compared to traditional animal-based products and $3.2 billion in investments since 2018.

As global leaders in alternative protein and plant-based food production, opportunities to expand food tech hubs in the Midwest, California, and Washington State are being supported by capital investments and venture capital funding.

Opportunities exist in other regions as well and will continue to present themselves in this growing, global market. While there is potential for cultured meat and plant-based alternatives to create market disruptions to traditional animal-based food production, there are also many opportunities for growth and sustainability by leveraging Food Tech hubs, upskilling the workforce, and innovating for affordability and sustainability.

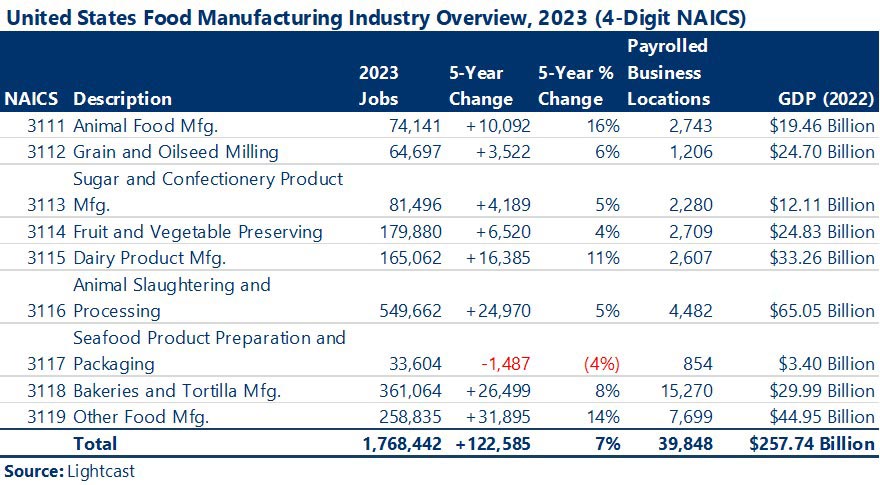

The Food Manufacturing sector accounts for over 1.7 million jobs across nearly 40,000 business locations across the United States as of 2023. The sector has posted strong job gains since 2018, adding over 122,000 jobs over this five-year period. This 7% growth outpaces the 4% growth experienced by the overall economy during the same time period.

Animal Slaughtering and Processing is the largest subsector and accounted for nearly one-third of employment in the Food Processing sector in 2023, with almost 550,000 jobs. Nearly all 4-digit subsectors saw employment growth over the last five years, with the sole exception of Seafood Product Preparation and Manufacturing. On a more detailed level, Meat Processed from Carcasses was the fastest-growing sub-industry from 2018-2023, adding over 19,000 new jobs (15%), followed by Retail Bakeries (+16,474 jobs, 16%). Traditional sources of industry data like those presented above indicate strong growth in animal-based food products in the United States. However, these traditional sources do not distinguish between plant-based and traditional animal-based products, making it difficult to identify fast-changing trends with this data alone.

Traditional sources of industry data like those presented above indicate strong growth in animal-based food products in the United States. However, these traditional sources do not distinguish between plant-based and traditional animal-based products, making it difficult to identify fast-changing trends with this data alone.

Other sources indicate an ongoing shift in consumer preferences towards plant-based alternatives. For example, the Good Food Institute’s analysis of 2022 SPINS data[1] indicates that the total value of plant-based sales at grocery stores increased by 7% year-over-year and a whopping 44% over three years.

This same data finds that plant-based milk accounts for about 15% of the total milk market in 2022, with 41% of households purchasing some type of plant-based milk throughout the year. Meanwhile, almost one in five households purchased plant-based meat in 2022. Notably, 93% of households that purchased plant-based meat that year also bought animal-based meat, indicating that consumers are introducing meatless alternatives to their diet gradually and may not be ready to go totally vegan yet, which is a much smaller market.

So, are these consumer trends impacting industry investing? In the last ten years, over $3.2 billion of capital investments[2] in these categories have been made in the United States. The plant-based category has by far the greatest dollar value of investment, topping $2.7 billion in the US.

Plant-based dairy products such as milk, yogurt, and cheese have attracted nearly $470 million in capital investment within the US in recent years. 2021 was the strongest year, with over $1.3 billion in the US across 21 separate projects.

The “other plant-based” category accounts for the most capital expenditure (capex), at $1.2 billion. This includes products such as snacks, energy drinks, protein powders, sauces, and more. This is closely followed by plant-based meat, which has garnered over $1 billion in investment during the last decade in the United States. This includes companies such as Impossible Foods and Beyond Meat, which produce meat-analog products out of plant-based materials.

Plant-based foods have generated the most investment in the last decade among the alternative protein categories, enjoying the longest and most consistent investment attraction among these categories in the US since 2018. However, other product segments have been quickly gaining momentum in recent years.

Cultured meat has attracted investments of nearly $250 million in 2022 and 2023 alone. This is an animal-based meat that is cultivated from real animal cells and grown in labs, rather than harvested from a slaughtered animal. Therefore, it is a slaughter-free protein, but not vegetarian.

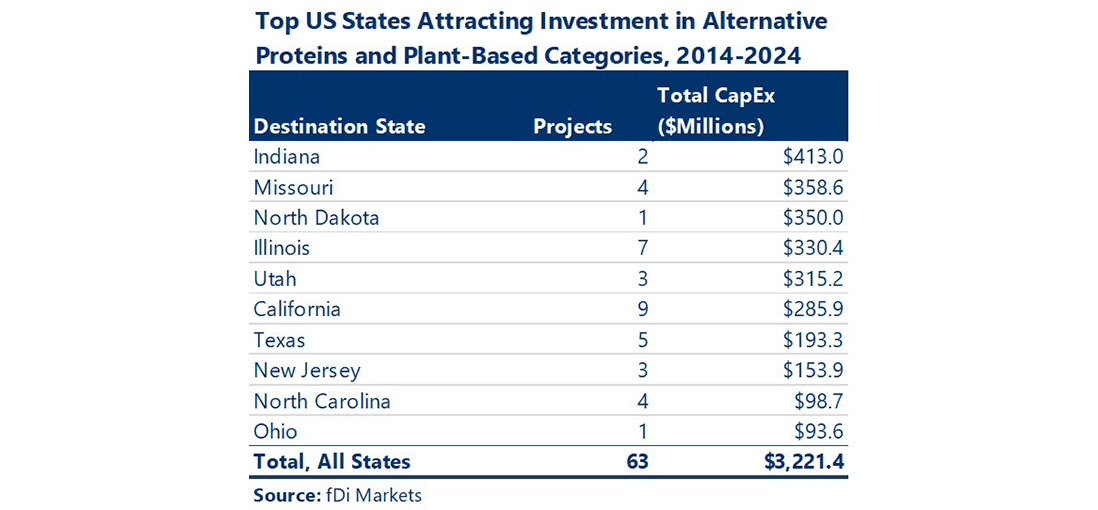

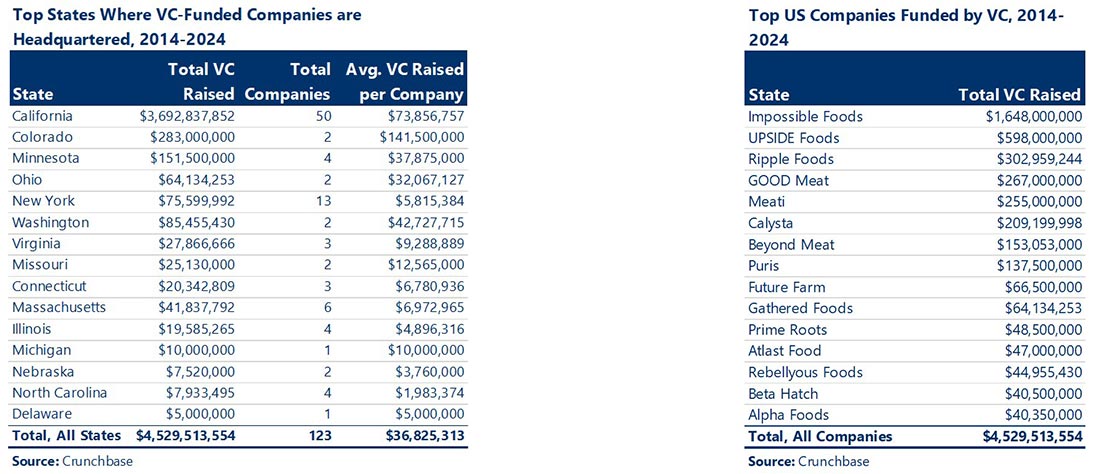

Geographically, four of the top five states for investment attraction are located in the Midwest. California and other Southern states also account for significant investment attraction in the last decade. Indiana has attracted the most money, with $413 million of investments since 2014, while California has attracted investment across the most projects — nine — for over $285 million in capex.

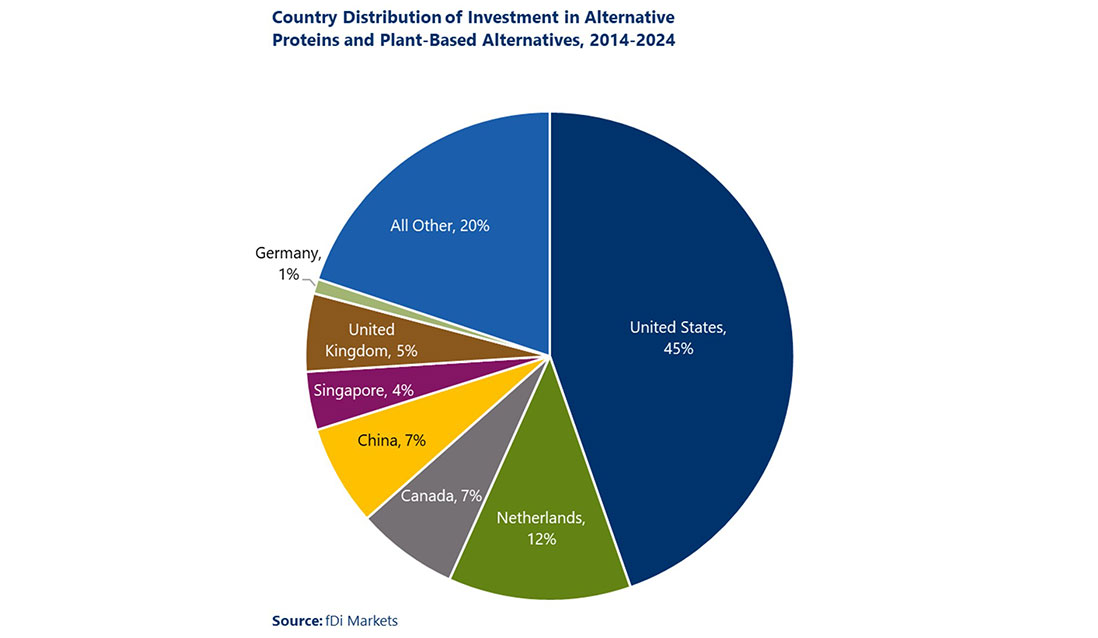

Globally, the US is the hub for investment in alternative protein and plant-based food production. In the last decade, 45% of all global capex have been directed at projects in the US. The countries with the next-highest total capex in these categories are the Netherlands, Canada, and China, which account for a combined 25% of total global capex in alternative proteins and plant-based foods.

The US also has a higher average capex per project, at $59.3 million on average per project compared to $42.7 million on average for the next five countries combined.

Venture capital (VC) transactions indicate that alternative proteins and plant-based foods is a fast-moving, high-growth industry.

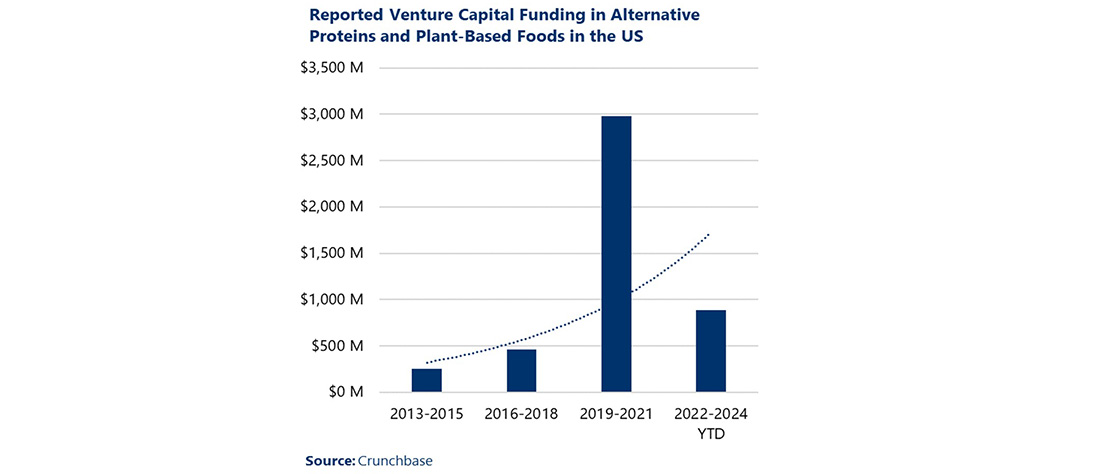

In the last decade, over $4.5 billion in VC funding has been raised by US-based startups in plant-based foods and alternative proteins, nearly $3 billion of which was raised during 2019-2021 alone. And unlike the capital expenditures data above, these investments were well underway at the start of the decade. This data suggests that the startup activity was primarily focused on building the industry in the early half of the decade, and that consumer markets grew sufficiently large to support market expansion in more recent years.

Notably, California accounts for almost 82% of the total VC funding raised in the last decade, with $3.7 million of total money raised across 50 startups.

The top three companies that have raised the most VC[3], Impossible Foods, UPSIDE Foods, and Ripple Foods, are headquartered in California close to funders, technology, and innovative universities but also within reasonable proximity regions where crops commonly used in plant-based food products are grown.

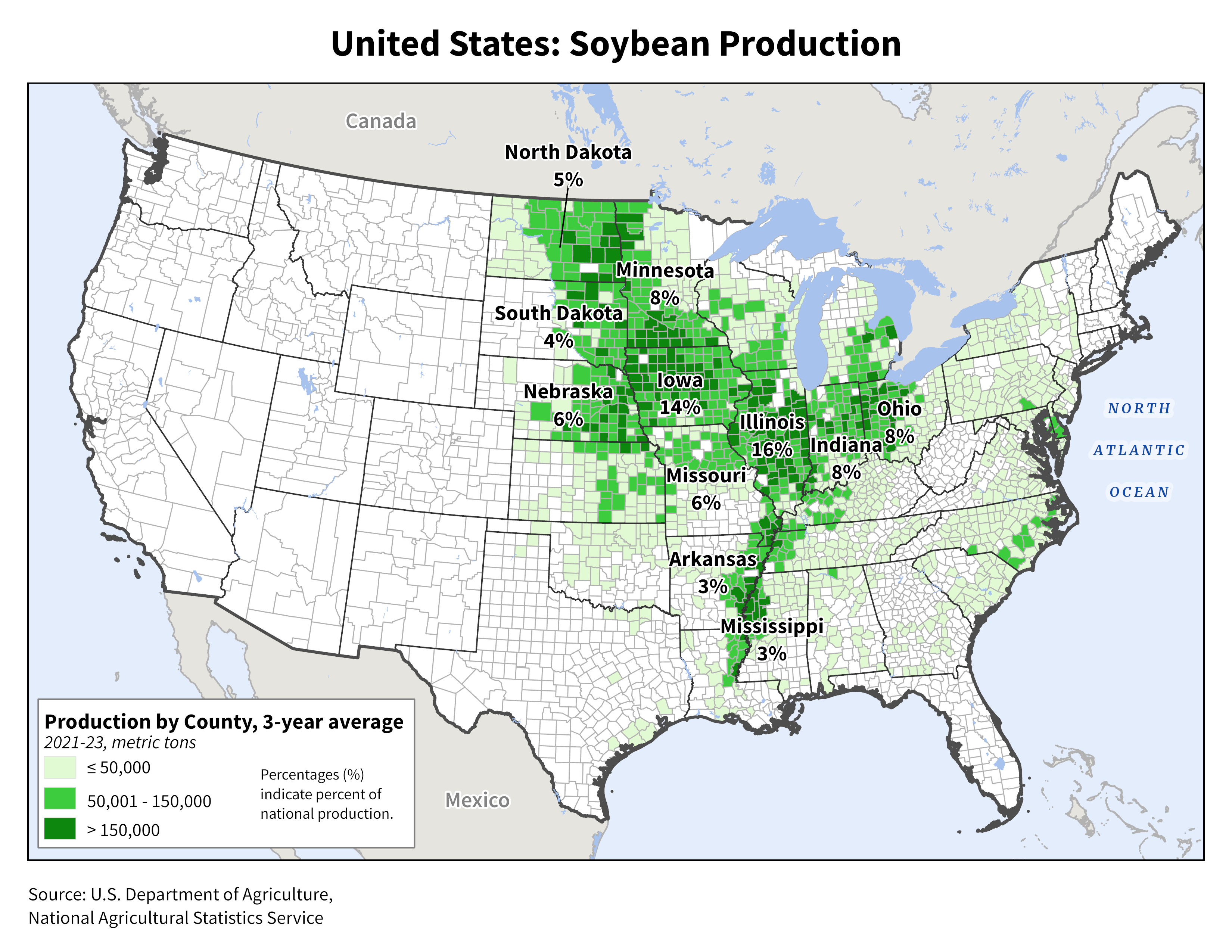

The base ingredients in plant-based foods and alternative proteins are commonly soy, chickpeas, wheat, lentils, peas, and potatoes. Those crops are primarily grown and harvested in the Midwest and Pacific Northwest. For example, 67% of US chickpea crops are produced in Washington and Montana,[4] and 27% of soybeans are produced in Iowa and Illinois.[5] Midwest states like Minnesota, Ohio, Missouri, Illinois, Michigan, and Nebraska also top the list as states with significant venture capital funding in the plant-based category since 2014.

Key highlights in recent US investments in the plant-based and alternative protein sector include:

Alternative protein and plant-based products have been driving new, large investments in the past ten years, despite a global pandemic and supply chain shortages across the nation.

Investing in food tech is a way to provide stable food options as the environment and economy change.

There are implications to this developing market which can potentially disrupt meat and dairy producers, but it also provides opportunities for economic growth and sustainability.

Two primary disruptions that can impact meat producers based on available market share are innovations in cultured meat and increasing access to plant-based alternatives.

Cultured meat competing for market share: If cultured meats become more cost-effective this might impact cattle and poultry producers because this increases accessibility and the competition for market share. Cultured meat can compete for market share similarly to real beef and chicken because it is not a vegetarian alternative, so it does not have as many replacement challenges like taste, texture, and overall experience when cooking.

Increasing market penetration of plant-based alternatives: Since 93% of households that purchase alternative proteins are omnivore households, this can disrupt the traditional meat producer market because non-vegans are consuming these products as well.

With growing investment and technological advances to change the type and quality of plant-based meats, there is a possibility that the market might shift away from historical consumption levels of traditional meat towards alternative proteins and plant-based products. This can have lasting negative implications on meat producers but offers new potential for agricultural producers to boost crops like soybeans, lentils, and chickpeas.

There are also multiple opportunities for growth like leveraging existing and growing food tech hubs, investing and upskilling the workforce, and innovating for affordability, accessibility, and sustainability.

Leveraging existing food tech hubs: The US is a leading powerhouse in alternative protein and plant-based investment, and this is an opportunity to leverage existing food tech hubs in the Midwest and California and grow the industry.

Economic developers can do this by supporting companies seeking to export value-added products domestically and overseas and by attracting businesses within this food sector’s supply chain to mitigate supply chain disruptions.

Changing workforce: While large investments are being made in food tech, there is an opportunity to train and upskill the workforce to support this growing industry. Food tech offers higher-paying jobs and needs a skilled workforce for long-term success in continued innovation and growth. Partnering with businesses and education institutions to better understand what the industry needs for success is a priority opportunity that communities can start working on now.

Innovating for affordable plant-based products and alternative proteins: One of the biggest challenges for plant-based foods and alternative proteins is the availability and cost of the product. This is primarily caused by to ingredient shortages and supply chain distributions due to distance, labor shortages, and global events (e.g., war in Ukraine, COVID-19, etc.).[6]

As additional capital investments are being made within this industry, there is the potential to create innovative processes that lower the cost of plant-based products and increase accessibility for all. This also directly relates to creating and using food tech in agriculture production to increase crop yields and better support the supply chain within the US (e.g., precision farming).

Sustainable product development and limiting waste: Beyond investment in alternative proteins and plant-based foods, there is a wider opportunity in the Food Sector to bridge gaps in product development with recycled products and with other adjacent industries. For example, Maine-based Marin Skincare uses lobster by-products that are typically discarded by the seafood processing industry as the key ingredient in its products. While Marin’s products are not vegan, data indicates that most households that purchase plant-based products (93%) across the US purchase both animal-based and plant-based goods.

Sustainability is likely to play a key role consumers’ purchasing decisions in the coming years, and companies’ ingenuity in promoting sustainable practices and limiting waste in food processing may help producers mitigate disruptions seen by other products perceived as more sustainable, like plant-based foods.

Learn more about Camoin Associates’ Industry Analytics and STRATEGY services

📍 Related Article:

Growth, Change Creates Opportunities in Food Manufacturing and Processing

[1] https://gfi.org/marketresearch/

[2] The fDi Markets database measures all cross-border investments that occur globally. This includes any capital investments occurring across state or country borders. However, this data does not capture any capital investment being made within the same state of a company’s headquarters.

[3] Venture Capital funding data is available for reported transactions only. Reporting is not required, and therefore not all transactions are included in this dataset.

[4] https://www.agmrc.org/commodities-products/vegetables/chickpeas

[5] https://ipad.fas.usda.gov/rssiws/al/crop_production_maps/US/USA_Soybean.png

[6] https://gfi.org/marketresearch/

Real Estate Development and Housing

Housing is essential infrastructure in rural communities, small towns, and micropolitan areas. It shapes workforce stability, economic resilience, and long‑term community viability. Explore case studies, actionable tools, and a step-by-step guide for meeting housing needs in these unique markets.

Industry Analytics and Strategy

Prospecting and Business Attraction

Your resource for understanding today and looking toward tomorrow

{kind=link}