- Navigator

- Agriculture and Forestry

- Expansion Solutions

- Industry Analytics and Strategy

Like all industries, forestry and lumber-related industries are experiencing significant transitions from global and national issues, including climate and related environmental changes, clean and green technology, demand for housing construction, labor market and demographics impacting workforce, and more. These issues are creating both opportunities and challenges. This article examines recent trends in and impacts on the forestry and lumber-related sectors and offers insights into emerging opportunities.

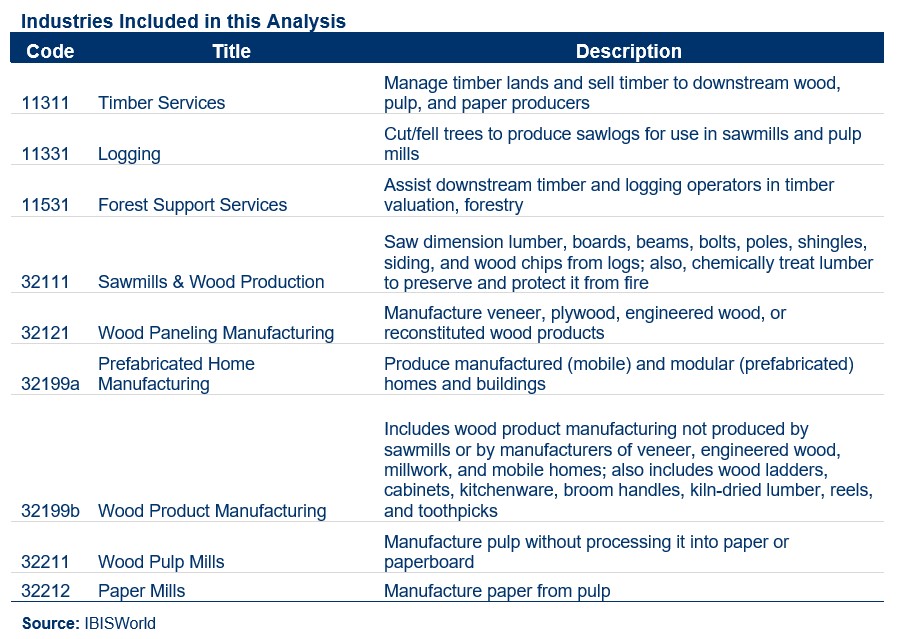

For the purposes of this article, forestry and lumber industries included in this article include services critical to the industry (timber services, logging, and other support services), Sawmills and Wood Product Production, and Pulp and Paper Manufacturing. A detailed list of these industry sectors is provided at the end of this article.

There were approximately 75,000 establishments in the forestry and lumber sector in 2022. Employment is heavily concentrated in the natural resources segment of the sector, with over 45,000 establishments in the logging industry alone and over 16,000 in the forest support services industry. Meanwhile, the lumber and wood products segment accounted for 10,500 business establishments in 2022.

Overall, the number of establishments in the sector dropped by 9% in the last five years and is projected to contract by another 6% through 2027. These reductions are driven by Wood Product Manufacturing and Logging, which lost a combined 8,700 establishments over the last five years.

Contractions across the board have been heavily influenced by high levels of foreign competition as the appreciating dollar has made exports less competitive. Other downstream impacts, like the declining production of Paper Mills, have had ripple effects throughout the industry.

Employment in the sector topped 425,000 in 2022, essentially unchanged from five years prior. Major employment reductions in industries like Paper Mills (-15,100) and Logging (-7,900) were offset by gains in Forest Support Services (+8,700), Sawmills and Wood Production (+8,350), and Prefab Home Manufacturing (+6,550).

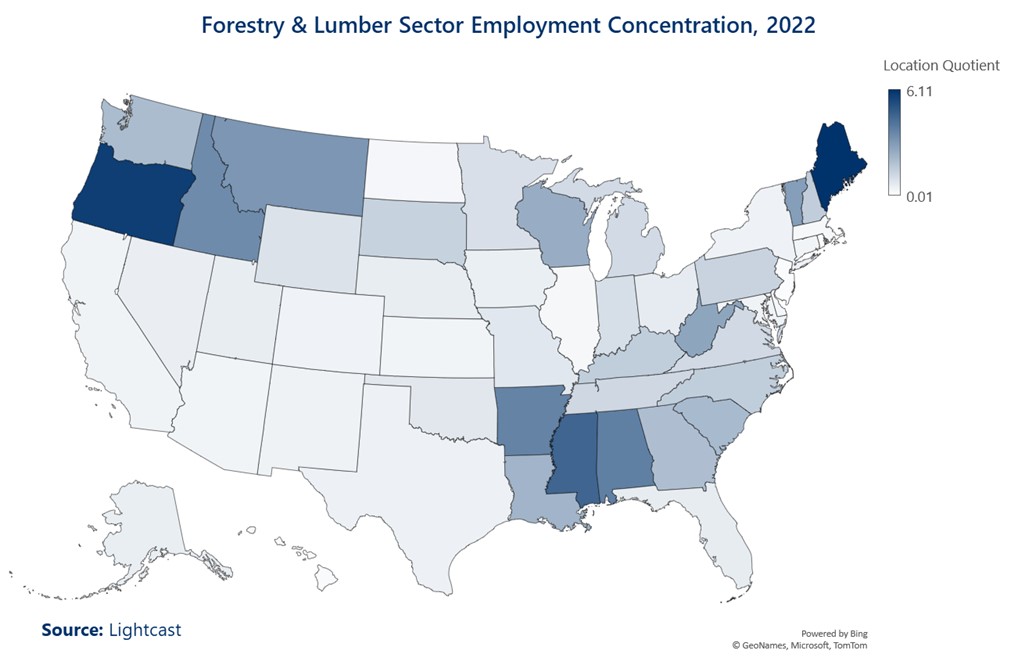

Despite relatively stable employment numbers over the last five years, employment is expected to decline by 7% over the next five years (-28,500 jobs). Nearly all sub-industries are expected to see a decline in employment through 2027. The sector is most concentrated in the Northeast, Pacific Northwest, and Southeast regions in the US. Maine has the highest employment concentration[2] (6.1), followed by Oregon (5.8), Mississippi (4.6), Alabama (3.8), and Arkansas (3.7).

The sector is most concentrated in the Northeast, Pacific Northwest, and Southeast regions in the US. Maine has the highest employment concentration[2] (6.1), followed by Oregon (5.8), Mississippi (4.6), Alabama (3.8), and Arkansas (3.7).

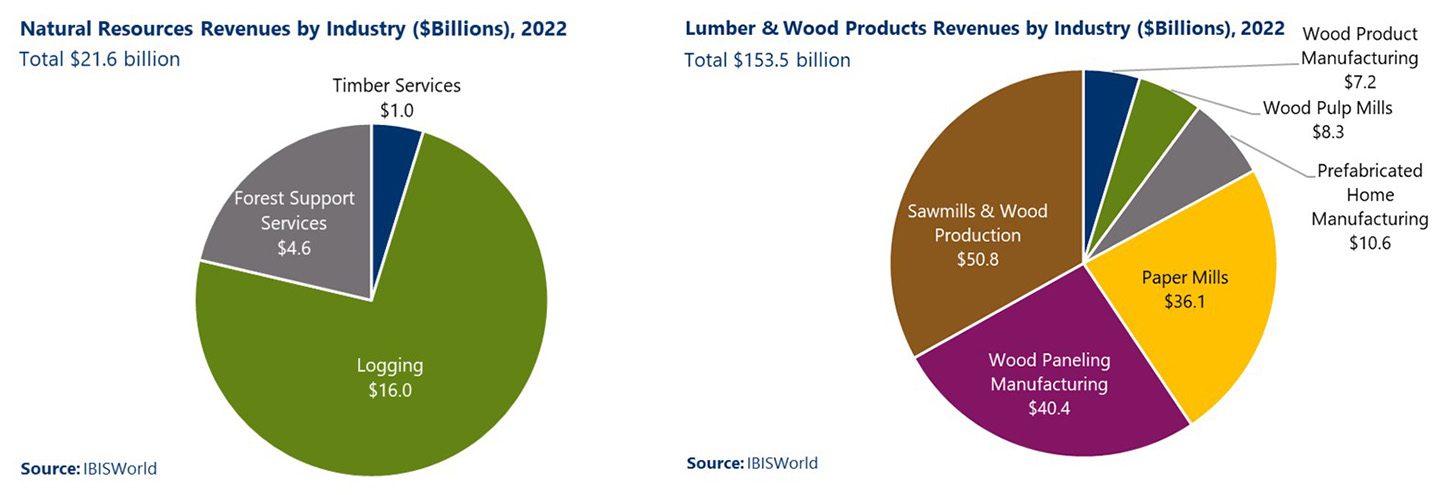

The natural resource segment of the sector (Logging, Timber Services, and Forest Support Services) had a total of $21.6 billion in revenue in 2022, while the lumber and wood products segment had a total of $153.5 billion.

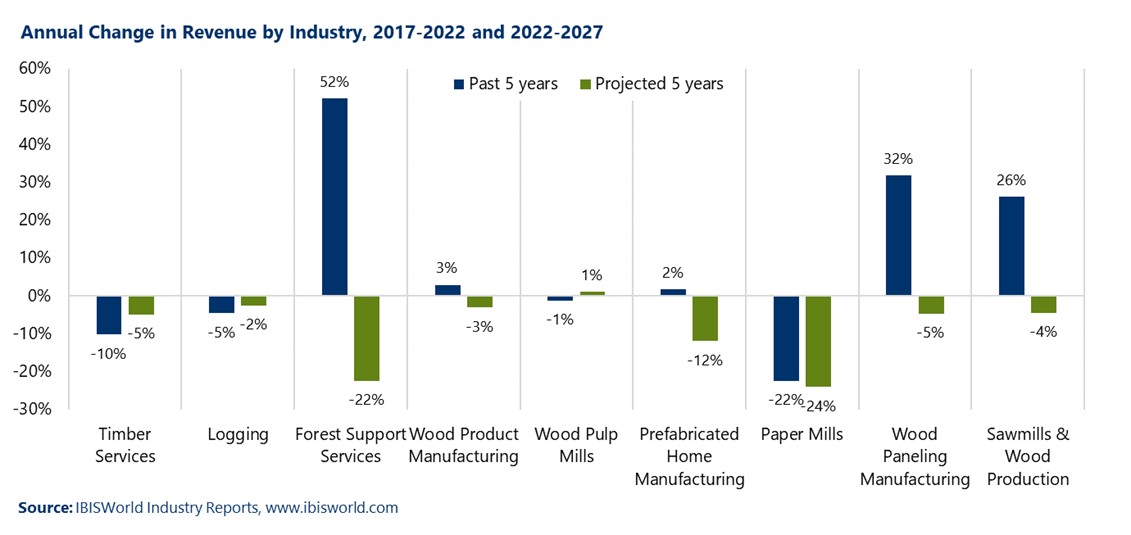

Logging was the largest natural resource industry by revenue, reaching $16 billion. Meanwhile, Sawmills and Wood Production; Wood Paneling Manufacturing; and Paper Mills together make up 83% of the lumber and wood products segment. In the past five years, the forestry and lumber sector’s revenue has grown by 7%. Some industries have seen significant declines, including Paper Mills (-22%), Timber Services (-10%), and Logging (-5%).

In the past five years, the forestry and lumber sector’s revenue has grown by 7%. Some industries have seen significant declines, including Paper Mills (-22%), Timber Services (-10%), and Logging (-5%).

During this period, losses were fully offset by gains in other industries, such as Forest Support Services (+52%), Wood Paneling Manufacturing (+32%), and Sawmills and Wood Production (+26%). Through 2027, the trend is projected to reverse. The sector’s revenue overall is projected to decline by 9% from 2022-2027, totaling a $15.7 billion decrease. Nearly every sub-industry is projected to see revenues contract, but declines are driven by Paper Mills, which is projected to see the most severe decline in revenue, dipping 24% or $8.7 billion.

The sector’s revenue overall is projected to decline by 9% from 2022-2027, totaling a $15.7 billion decrease. Nearly every sub-industry is projected to see revenues contract, but declines are driven by Paper Mills, which is projected to see the most severe decline in revenue, dipping 24% or $8.7 billion.

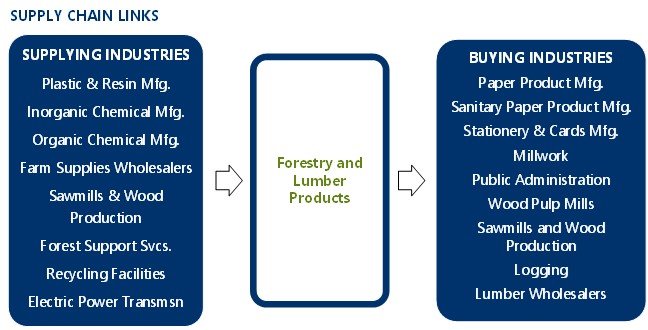

The forestry and lumber sector has strong intra-industry supply chain linkages, with industries like Sawmills and Wood Production and Forest Support Services being both suppliers and buyers of the industry’s products. Other important buyers include Paper Product Manufacturing, Public Administration, Wood Pulp Mills, Logging, and Lumber Wholesalers.

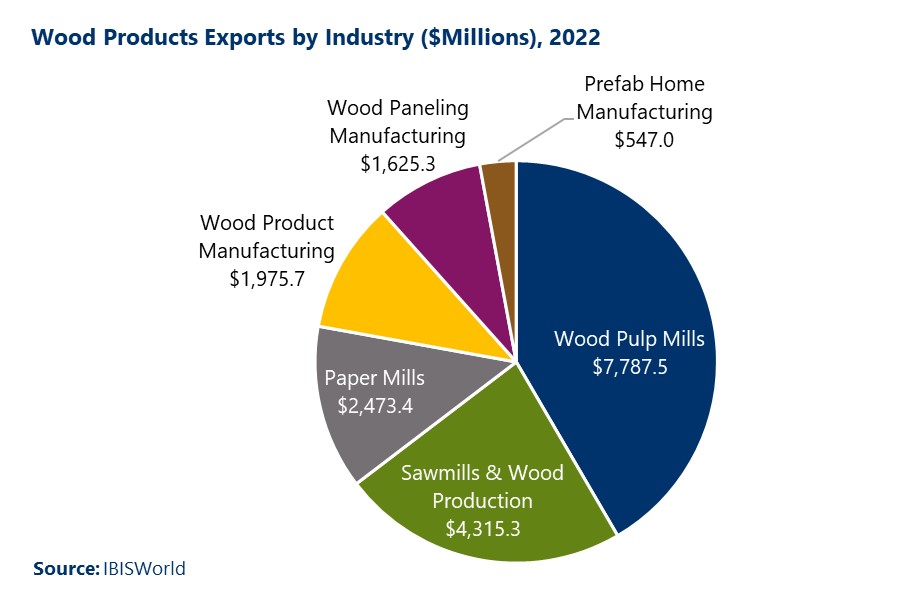

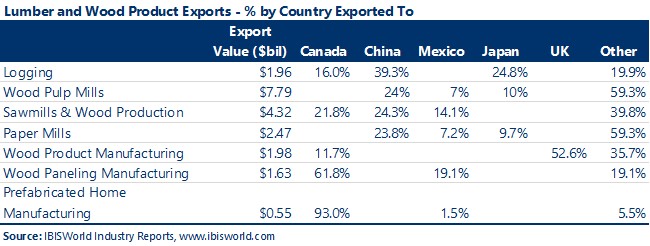

Wood Pulp Mills exported $7.8 billion to foreign partners in 2022, accounting for 38% of all foreign exports in the lumber and wood products segment of the sector. Other major exporting industries include Sawmills and Wood Production ($4.3 billion) and Paper Mills ($2.5 billion). China and Canada are the United States’ two largest export partners for the forestry and lumber sector, accounting for approximately $4.3 billion and $3 billion of exports in 2022, respectively. Other nations such as Mexico, Japan, and the United Kingdom represent major trade partners.

China and Canada are the United States’ two largest export partners for the forestry and lumber sector, accounting for approximately $4.3 billion and $3 billion of exports in 2022, respectively. Other nations such as Mexico, Japan, and the United Kingdom represent major trade partners.

There are multiple key economic variables that influence the market performance of the forestry and lumber sector. These include:

Below is an overview of the strongest drivers of the industry.

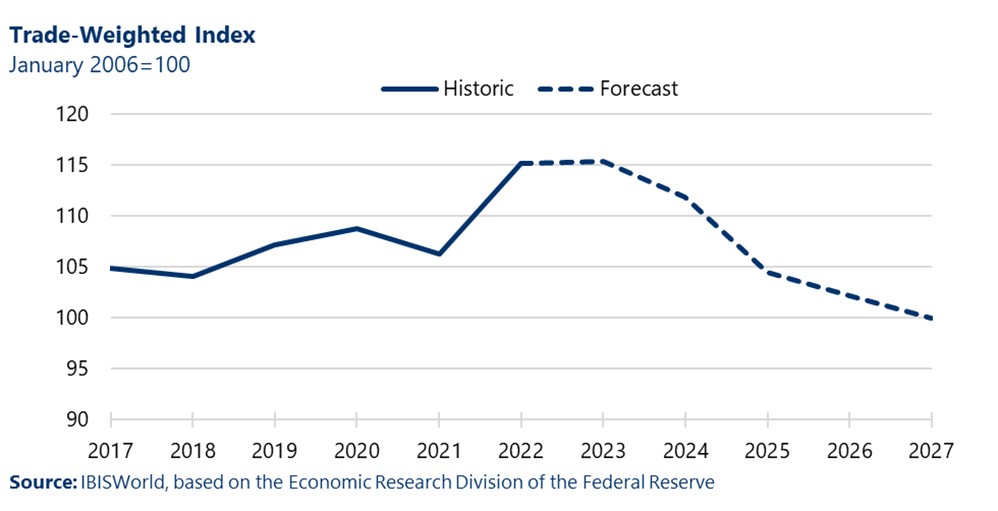

The Trade-Weighted index, otherwise known as the Nominal Broad US Dollar Index, measures the strength of the US dollar compared to the currency values of the nation’s trading partners and is calculated by comparing exchange rates to the magnitude of trade with other nations. When the Trade-Weighted Index is higher, the relative value of the dollar is stronger, meaning exports are less competitive in the global market.

While the index increased in 2022, it is expected to gradually decline through 2027. A lower trade-weighted index in the coming years would improve the competitiveness of the United States’ exports, creating further opportunities for the forestry and lumber sector to access international markets.

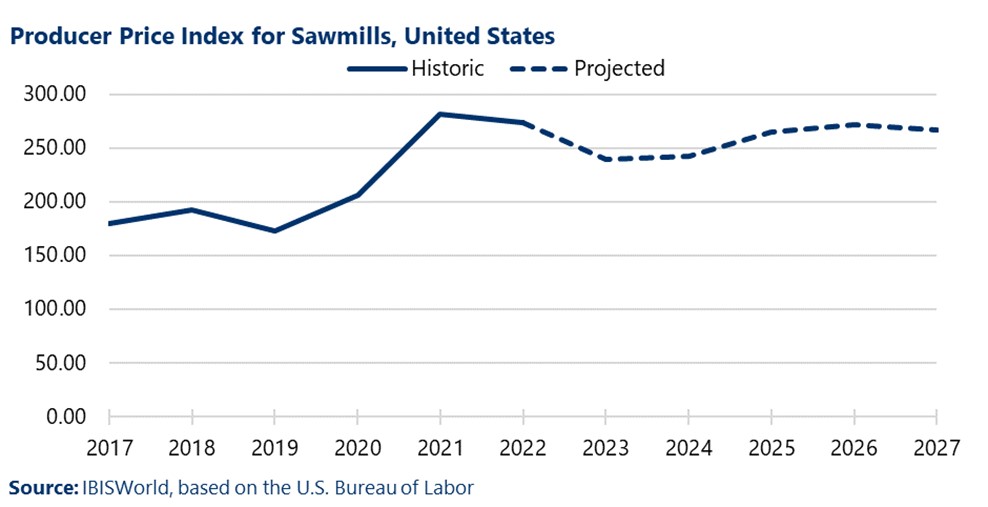

The price of sawmill lumber has competing impacts on different segments of the forestry and lumber sector. While rising prices serve as a boost to revenues for industries like Logging and Sawmills, it deals a short-term blow to industries like wood product manufacturing that use lumber as a primary input.

The price of sawmill lumber has been somewhat volatile in recent years, spiking through 2021 and growing 52% from 2017-2022. Over the next five years through 2027, prices are expected to remain somewhat stable, declining slightly by 2%.

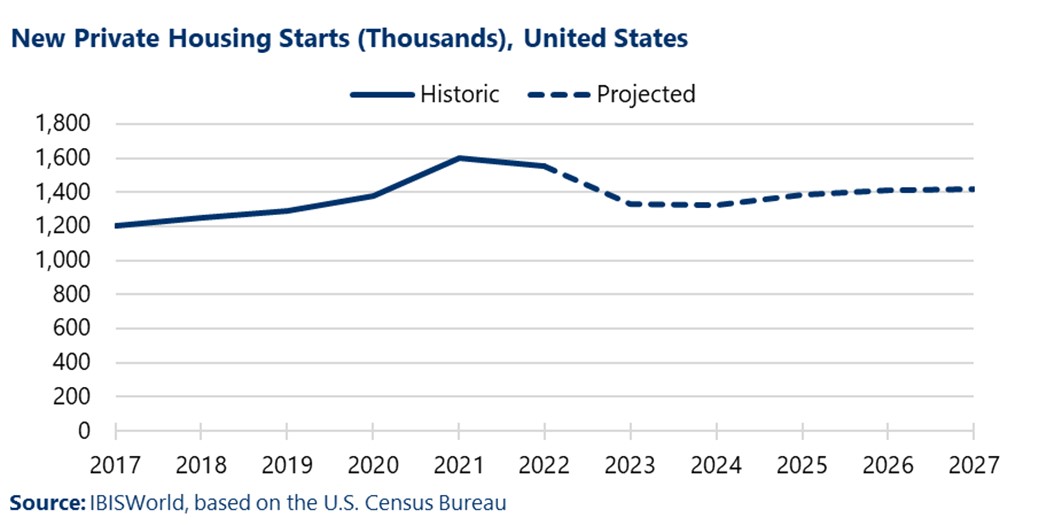

Housing starts represent the number of new privately-owned housing units that started construction during the year, including both single-family and multifamily units. Housing starts are a good indicator of demand for residential building materials and lumber. Housing starts spiked in 2021, reaching 1.6 million units amid the COVID-19 pandemic and favorable borrowing conditions. However, starts are expected to decrease in 2023 and slow in the next five years as the housing market cools. Additionally, high interest rates are creating unfavorable borrowing conditions for homeowners and home builders.

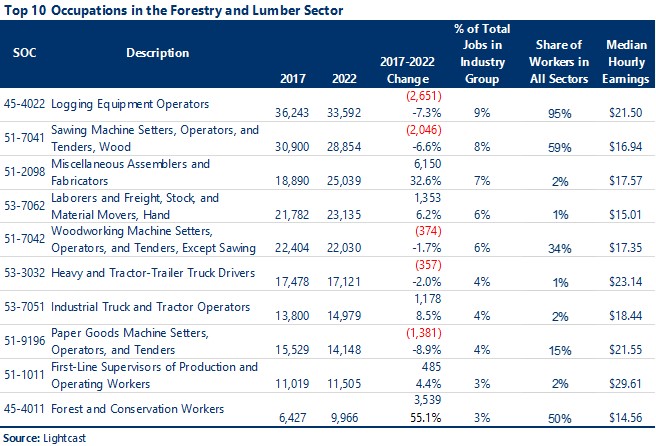

Workforce is a major challenge to stability and growth in the forestry and lumber-related sectors. In 2022, the top occupation in the sector was Logging Equipment Operators, which accounted for 33,592 jobs and 9% of total employment in the sector in 2022. Individuals who work in this occupation operate a wide range of equipment but tend to operate heavy machinery used in forestry activities. Overall, 95% of Logging Equipment Operators work in forestry and lumber. However, other top occupations are not as concentrated within the sector. In fact, many of the top occupations face significant competition for labor across other industries. These include Laborers and Freight, Stock, and Material Movers or Heavy and Tractor Trailer Truck Drivers, with about 1% of these workers in the forestry and lumber sector.

However, other top occupations are not as concentrated within the sector. In fact, many of the top occupations face significant competition for labor across other industries. These include Laborers and Freight, Stock, and Material Movers or Heavy and Tractor Trailer Truck Drivers, with about 1% of these workers in the forestry and lumber sector.

Heavy and Tractor-Trailer Truck Drivers, for example, were the sixth-most in-demand occupation over the last 60 months[3], with over 4 million unique job postings. Laborers and Freight, Stock, and Material Movers represented the eighth-most in-demand occupation during the same time period, with 3.4 million unique job postings. This being said, the forestry and lumber sector faces steep labor competition for its top occupations and likely will continue to struggle to fill these roles in the near future.

The forestry and lumber sector will face various challenges in the next several years, which it will need to overcome in order to see growth.

Despite these challenges, several new opportunities exist on the horizon for the forestry and lumber sectors.

Currently, mass timber is more commonly used in the Midwest and Pacific Northwest, though recent activity, including in Maine, is occurring in the Northeast.

Focusing on forest and lumber products for targeted business and economic development is not for every area. A region must have reasonable proximity to forest land.

However, while the Northeast, Pacific Northwest, and Southeast have high concentrations for forest land, other areas of the country have some forest areas and/or proximity to lumber and wood-related product inputs.

In supporting and growing opportunities in these sectors economic and business developers should:

| Product Trade Shows | |

| Sector for Show | Name of Show |

| Machinery and Equipment | Forest Products Machinery and Equipment Expo |

| Machinery and Materials | Holz-Handwerk |

| Millwork | Timber Processing and Energy Expo (TP&EE) |

| Pulp and Paper | Fastmarkets Forest Products North America Conference |

| Timber | International Mass Timber Conference |

| Woodworking | AWFS Fair |

| Woodworking | International Woodworking Fair (IWF) |

| Woodworking | IWPA World of Wood Convention |

| Woodworking | Ligna Hannover: World Trade Fair |

| Woodworking | Wood Pro Expo Illinois |

| Woodworking | Wood Pro Expo Lancaster |

Learn more about Camoin Associates’ Industry Analytics + Strategy Services

Learn more about Camoin Associates’ Industry Analytics + Strategy Services

[1] Unless otherwise noted, data for this section is derived from forestry and lumber economic performance from IBIS World Industry Reports, www.ibisworld.com. Data is for 2022 and represents 12-month data unless otherwise specified.

[2] Concentration is measured by location quotient (LQ), which compares the concentration of employment in an industry within a state to the overall concentration of the industry’s employment nationally. Values greater than 1.0 indicate that the industry is more concentrated in the state than on the national level.

[3] June 2018-June 2023

[4] Research conducted at the USDA Forest Products Laboratory (Madison, WI) indicates the superior strength of un-milled timbers. SDRT are 50% stronger in bending than an equivalent square section of milled lumber (Wolfe, 2000)

[5] Manufacturing Facility Feasibility Analysis, November 2022, Camoin Associates prepared for the Town of Ashland, ME, and Original Mass Timber Maine (OMTMaine)

[6] Murray, Lara and Androff, Amy. “The Greener World of Tomorrow: Build with Revolutionary Wood Products,” US Forest Service. 21 Oct 2021.

[7] Monthly Energy Review, April 2023, U.S. Energy Information Administration

Economic and Fiscal Impact Analysis

A recent analysis of a digital equity program in Westchester County, NY, revealed that it generated outsized economic benefits and return on investment for the community.

Business Retention and Expansion (BRE)

Industry Analytics and Strategy

Your resource for understanding today and looking toward tomorrow