- Navigator

- Expansion Solutions

- Industry Analytics and Strategy

- Prospecting and Business Attraction

- Information Technology, Semiconductors, and AI

This article originally appeared in the October 2025 issue of Expansion Solutions magazine.

Semiconductors are now strategic infrastructure. Once a behind-the-scenes industry, chip manufacturing has become a central pillar of economic competitiveness and national security, prompting major public and private investments in domestic production.

Employment and investment in the semiconductor industry are surging. Between 2019 and 2024, the US Semiconductor industry added over 33,000 jobs—outpacing broader economic growth—and is driving demand for both high-skill engineering talent and accessible production roles.

Site selection is being reshaped by power, speed, and talent. Semiconductor companies increasingly prioritize regions with reliable, affordable energy, ready-to-build industrial sites, and strong university-to-industry talent pipelines—benefiting areas in the Southeast and Midwest.

Peoria, AZ, is one example of proactive planning in an effort to attract investment by the Semiconductor industry. Through strategic land and infrastructure investments, Peoria has transformed into a semiconductor hub, leveraging partnerships, workforce programs, and infrastructure readiness to attract global players like Amkor and TSMC.

Semiconductors are the microscopic engines powering the global economy. These microelectronic components, commonly referred to as chips, are essential to everything from smartphones and vehicles to medical devices, defense systems, energy infrastructure, and advanced manufacturing. As foundational technology, semiconductors enable innovation across nearly every sector, making their availability and advancement critical to both economic competitiveness and national security.

In recent years, the Semiconductor industry has moved from behind the scenes to center stage. Disruptions caused by the COVID-19 pandemic, geopolitical tensions, and surging global demand have exposed vulnerabilities in supply chains and underscored the need for greater domestic production capacity. In response, the United States and its economic development partners have mobilized around federal incentives, reshoring initiatives, workforce training programs, and innovation ecosystems aimed at supporting the next generation of semiconductor technology.

This article explores the evolving semiconductor landscape, the factors driving site location, industry growth, and the opportunities it presents for regions seeking to attract advanced manufacturing and technology jobs.

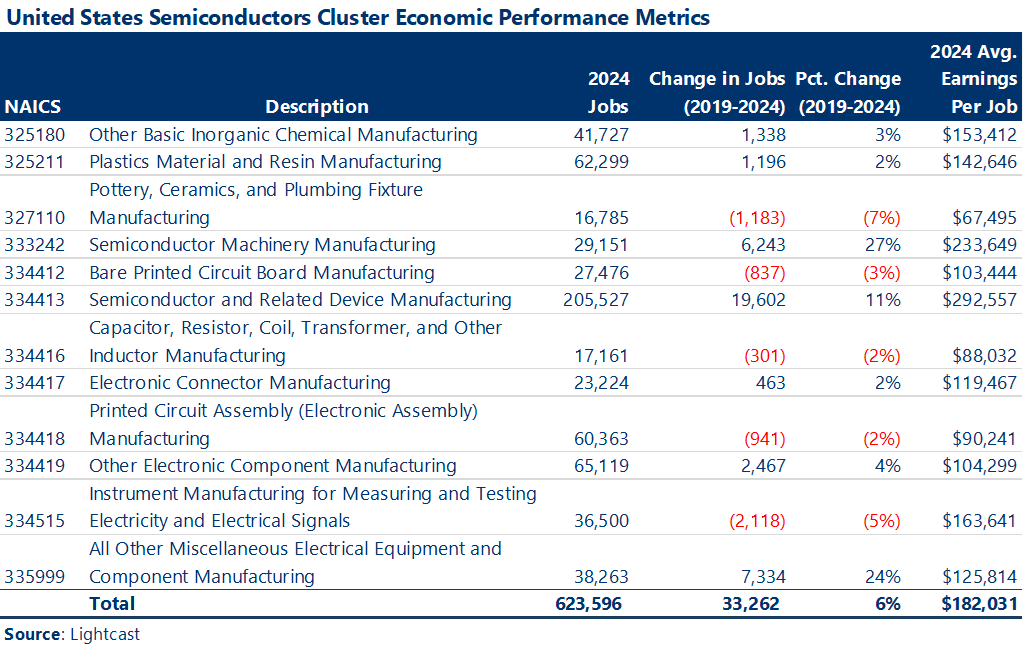

The US Semiconductor industry is entering a period of accelerated growth, reshaping the talent landscape for communities across the country. According to Lightcast, jobs in the Semiconductor cluster increased by over 33,000 between 2019 and 2024, a nearly a 6% increase, reaching a total of approximately 624,000 jobs in 2024 (Note: For this article, we define the cluster as focused on production and manufacturing of chips, excluding warehousing, packing, or research components). This growth outpaces many other manufacturing sectors as well as the overall US economy, which grew by 4% during the same period.

While the average earnings per job in the industry exceeded $182,000 in 2024, there is a wide range of opportunities available for various skill levels (Source: Lightcast). The growing number of entry points has mobilized career centers, community colleges, and universities to create pathways into semiconductor careers. Production occupations, which make up nearly 40% of all jobs in the sector, added approximately 11,000 new positions from 2019 to 2024 (Source: Lightcast). These technician and assembly roles offer accessible entry points to high-paying careers that can be scaled through continued training.

From the early CHIPS Act buzz of 2021 through the supply chain reset of 2025, Camoin Associates’ semiconductor prospect pipeline has charted a sustained surge in activity. Our prospecting work highlights a two-tiered expansion pattern that remains highly relevant:

Key location drivers for both tiers include:

Those requirements, in turn, are reshaping the map. Half of our prospects are Silicon Valley or Southern California firms actively considering redirecting growth to the Carolinas, the Southeast, and the Ohio Valley. These are regions that pair lower electricity rates with right-to-work labor markets and strong technical-college pipelines.

While employment in the US Semiconductor industry grew by 4% over the last five years, Arizona’s Semiconductor sector expanded by 16% over the same period, growing roughly four times faster than the nation. The City of Peoria is a prime example of how targeted investments and long-range planning enabled the city to secure investment and emerge as a hub in the national (and global) semiconductor value chain.

Anchored by a $2 billion investment from Amkor Technology, the largest outsourced semiconductor packaging facility in the US, Peoria is positioning itself as a hub for advanced manufacturing and supply chain innovation. The facility will package and test chips for TSMC’s nearby fabs and is expected to create over 2,000 jobs, underscoring the region’s growing role in post-fabrication operations.

To support this surge, the City of Peoria has launched an ambitious land and infrastructure strategy centered around an 834-acre site known as Core 2. Through an intergovernmental agreement (IGA), the city is fronting $140 million in infrastructure investment, with reimbursement expected from future land sales through Arizona’s State Land Trust. The site is already attracting strong interest from semiconductor and clean tech suppliers and has a groundbreaking scheduled for October.

The city’s strategic advantages are numerous:

Peoria’s transformation from a bedroom community to a dynamic innovation hub also reflects thoughtful land-use planning, housing diversification, and strategic infrastructure readiness. However, local leaders are also candid about the challenges: power and water resources are under pressure from competing demands, which is the impetus for Peoria’s ambitious infrastructure commitments.

With Amkor, TSMC, and other global players staking claims in the region, Peoria stands as a model for how secondary markets can leverage land, infrastructure, and intergovernmental partnerships to unlock high-value foreign direct investment in the semiconductor sector.

“Peoria is investing hundreds of millions of dollars to prepare the entire Peoria Innovation Core and Core 2 for advanced manufacturing development. This investment supports the creation of community amenities and educational facilities ensuring the area is shovel-ready for growth. Construction is already underway on road, sewer, and wastewater infrastructure as we prepare for Amkor Technology to break ground in October.”

As the Semiconductor industry evolves, economic developers play a critical role in shaping where and how expansion occurs. Their ability to negotiate effectively with businesses and highlight community assets can directly influence site selection outcomes.

Key takeaways include:

📍 Related Article:

Bridget Byrnes is an Economic Data and Research Analyst at Camoin Associates. She holds a Bachelor of Arts in Writing from Emerson College and a Master of Public Administration with a concentration in economic development from Murray State University. As an analyst, Bridget leads data-driven research and strategic planning initiatives across housing, industry, and economic and fiscal impact projects. She has guided efforts ranging from housing and market analyses in communities across the Northeast to cluster and workforce analyses that help regions position themselves for long-term competitiveness. Bridget works closely with local leaders to translate complex economic and demographic data into actionable strategies that support inclusive growth and sustainable development.

Dillion Roberts is the Director of ProspectEngage® at Camoin Associates. He has a Bachelor of Science degree in Technology Systems with an emphasis in Technical Management from from Utah State University and a minor in Business Management and Leadership through the Huntsman School of Business. With over 16 years of versatile expertise in project management, sales, marketing, and client account stewardship, Dillion is a seasoned professional adept at fostering economic development and driving transformative change. Drawing upon his extensive industry experience, he goes beyond the conventional, spearheading business attraction initiatives that fuel growth and innovation.

Alexandra Tranmer, CEcD, is the Director of Industry and Workforce at Camoin Associates. She has an Honors Bachelor of Arts degree and a Master of Science degree in Planning (MScPl) from the University of Toronto in Ontario, Canada. As a senior project manager, Alex has led complex strategic planning efforts in geographies ranging from bustling urban centers to pastoral tourist destinations, requiring adept stakeholder management and collaboration. She works with clients to balance the competing interests of stakeholders while ultimately helping them develop an ambitious yet achievable plan under their current organizational climate.

Learn more about our Industry Analytics and Strategy services

Learn more about our Prospecting and Business Attraction services

Economic and Fiscal Impact Analysis

A recent analysis of a digital equity program in Westchester County, NY, revealed that it generated outsized economic benefits and return on investment for the community.

Business Retention and Expansion (BRE)

Industry Analytics and Strategy

Your resource for understanding today and looking toward tomorrow