- Navigator

- Business Retention and Expansion (BRE)

- Industry Analytics and Strategy

- Manufacturing

Navigating today’s global economic landscape requires more than just reacting to change—it demands a clear understanding of your assets, your vulnerabilities, and where you are primed to maximize your assets.

Navigating today’s global economic landscape requires more than just reacting to change—it demands a clear understanding of your assets, your vulnerabilities, and where you are primed to maximize your assets.

Whether you are a business leader, policymaker, or economic development professional, one of the most important tools you can use to make sense of uncertainty is a risk assessment. This is not about predicting the future or trying to game the system. It’s about identifying where you are most exposed, understanding the implications of that exposure, and developing a plan to adapt and, when the time is right, emerge stronger.

At Camoin Associates, we’ve spent the last 25 years helping communities across the country respond to and recover from a wide range of disruptions—from plant closures and environmental disasters to pandemics, supply chain breakdowns, and evolving trade policies.

These events all underscore a fundamental truth: Economic shocks are inevitable, but the ability to respond quickly and strategically can make all the difference.

Risk assessments are at the heart of resilience planning. With the right data, a willingness to collaborate, and an understanding that uncertainty is here to stay, businesses and communities can prepare for a range of possible futures. This approach enables not just survival, but transformation—identifying new market opportunities, reducing reliance on vulnerable systems, and building long-term economic strength.

As economic development organizations (EDOs) work to support the complex web of industries, businesses, and communities in their regions, understanding the impact of shifting trade policies is critical. Are local businesses heavily involved in exports? Do you know what products are being shipped, where they’re going, and how they get there?

Without this foundational knowledge, it’s nearly impossible to assess how changes in tariffs or global demand could ripple through your local economy.

In this article, we examine risks in the context of trade and tariffs and demonstrate why a risk assessment is imperative for any community, EDO, or economic developer looking to get their house in order so they can weather uncertain economic times.

Access to recent and reliable data is a critical component to properly assessing a location’s risks. One component of Camoin Associates’ data toolbox includes IBISWorld’s US Trade Tariff Exposure tool.

This tool provides a model that helps clarify the geographical impacts of tariffs and potential risks to the supply chain and market access. It also provides industry-level analysis that measures an industry’s reliance on both foreign suppliers and foreign buyers as a share of total demand and total sales in key trade partner countries such as Mexico, Canada, China, the European Union, and others.

To demonstrate how trade dynamics influence local economies and business resiliency, we chose three industries that are highly interconnected with national and global markets. They serve as valuable examples of how trade policy, supply chain shifts, and domestic market access can affect production, distribution, and business growth:

This industry includes the development and production of prescription and over-the-counter medications, biological products, and therapeutic preparations.

With globalized supply chains for raw ingredients and heavy reliance on regulatory compliance across markets, it is sensitive to changes in international trade policy and supply chain disruptions.

This industry produces a wide range of plastic goods used across industries, including packaging, construction materials, consumer products, and components for medical and automotive equipment.

Its trade exposure stems from both the import of raw inputs, like natural gas, crude oil, and cellulose and the export of finished products, making it a key indicator of how industrial supply chains react to shifting domestic and international demand.

This industry produces surgical instruments, orthopedic devices, hospital furniture, and other medical and dental equipment.

Due to its role in public health and dependence on domestic distribution networks and global supply chains, it highlights the importance of timely trade logistics, regulatory alignment, and flexible sourcing and market strategies.

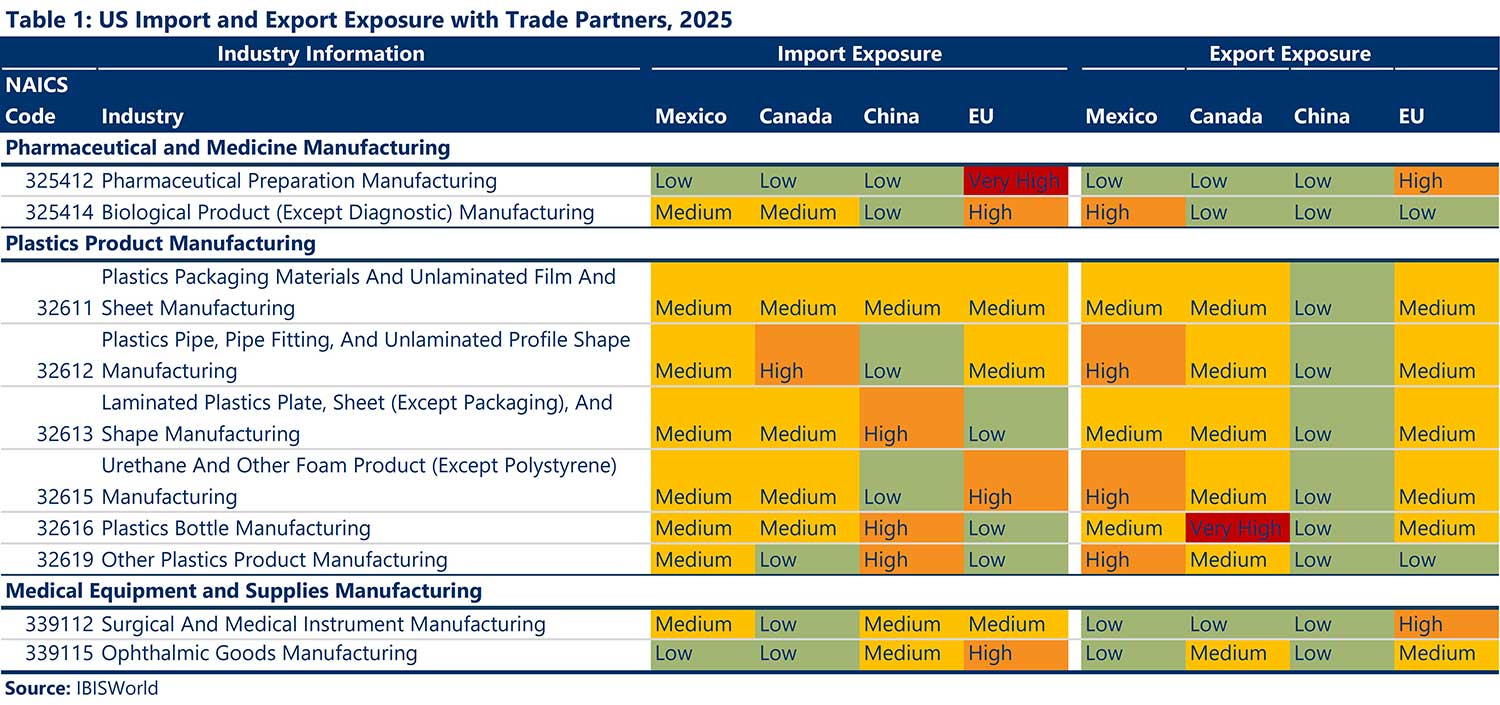

Table 1 below shows varying levels of risk within import and export markets of subindustries. Red indicates high risk, yellow, medium risk, and green, a lower risk.

Table 2 below quantifies the United States’ 2024 trade performance across these major global trade partners. The data reveals varied trade dynamics, underscoring where the US holds competitive advantages and where vulnerabilities exist.

The US maintains strong trade surpluses across most partners, especially with the European Union, where exports far exceed imports by over $100 billion.

Canada and China also show positive balances, though at a much smaller scale, reflecting steady demand for US pharmaceutical products.

The only notable deficit in this industry is with Mexico, where imports surpass exports by approximately $2.5 billion.

The trade picture shifts significantly in the plastics products industry. Here, the US faces substantial trade deficits with China and Mexico, most notably a $15.5 billion gap with China, highlighting the dominance of Chinese plastic goods in the US market.

Only modest surpluses are recorded with Canada and the EU, suggesting limited global competitiveness or insufficient domestic production in this category.

In contrast, the medical equipment and supplies industry is more favorable for US trade. The US has stronger surpluses with Mexico and Canada, indicating a robust export market for US-produced medical technologies and devices.

However, a significant deficit with China persists, suggesting reliance on Chinese medical equipment imports.

The European Union reflects a relatively balanced trade relationship, with a small surplus in favor of the US.

With the national perspective of imports/export activity, let’s dive further into a state-by-state analysis of where these industries employ the greatest proportion of people across the US using employment concentration data.

Employment concentration is a measure of industry concentration within a region. An employment concentration of 1.0 means that an industry is as concentrated within the region as it is on a national level. An employment concentration greater than 1.0 indicates that an industry is more concentrated in a region than at the national level.

The three chosen industries contribute significantly to employment, innovation, and overall economic activity across the country. Disruptions in any one of these industries could have cascading effects across health systems, manufacturing networks, and consumer markets.

With additional data, we can better understand what parts of the US are at risk based on the concentration of these industries across the nation.

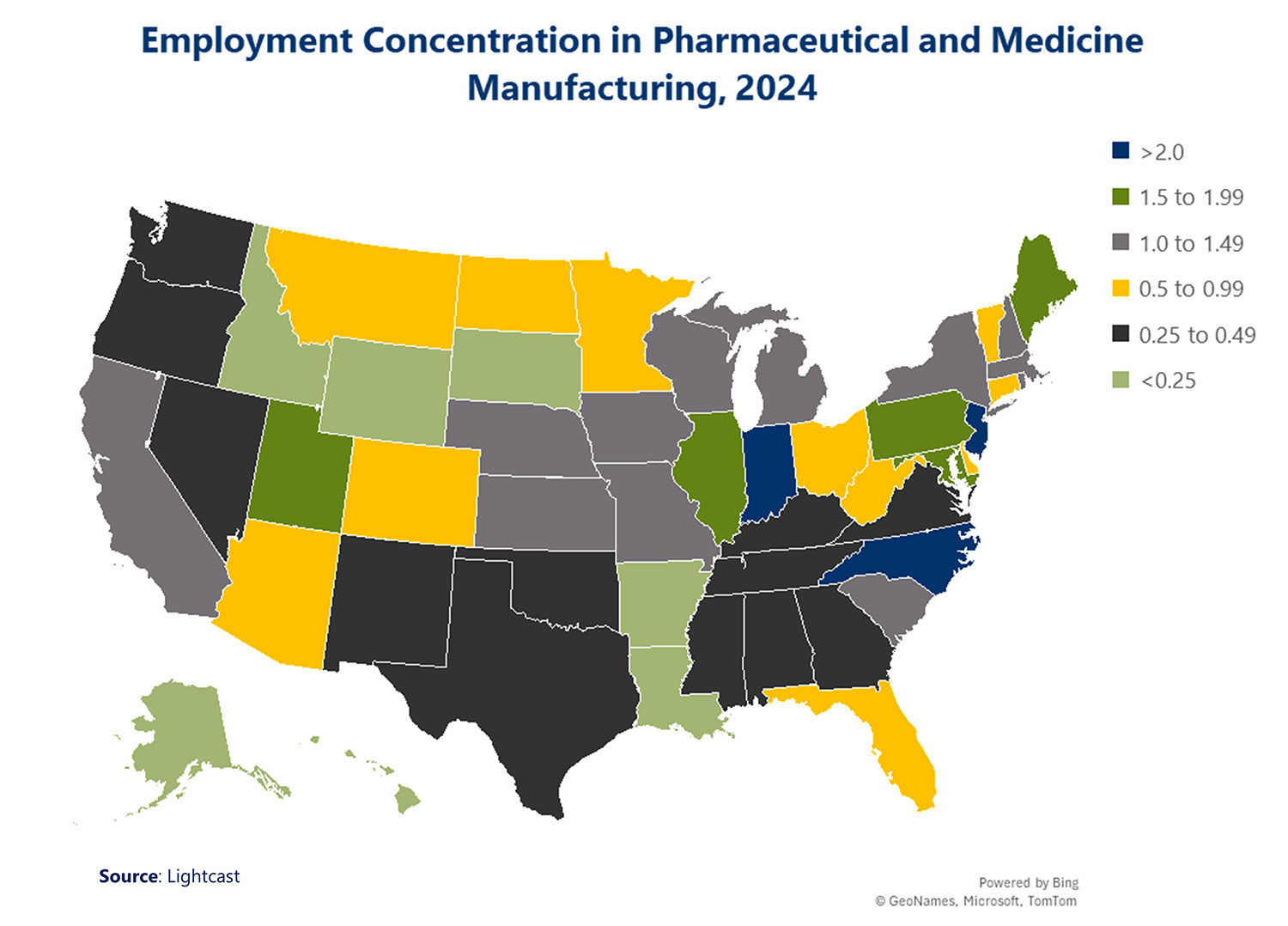

New Jersey, Indiana, and North Carolina are twice as concentrated in Pharmaceutical and Medicine Manufacturing as the US.

For example, in New Jersey, Indiana, and North Carolina, about 1% of total employment within the state is in Pharmaceutical and Medicine Manufacturing, compared to less than 0.5% of total employment throughout the US.

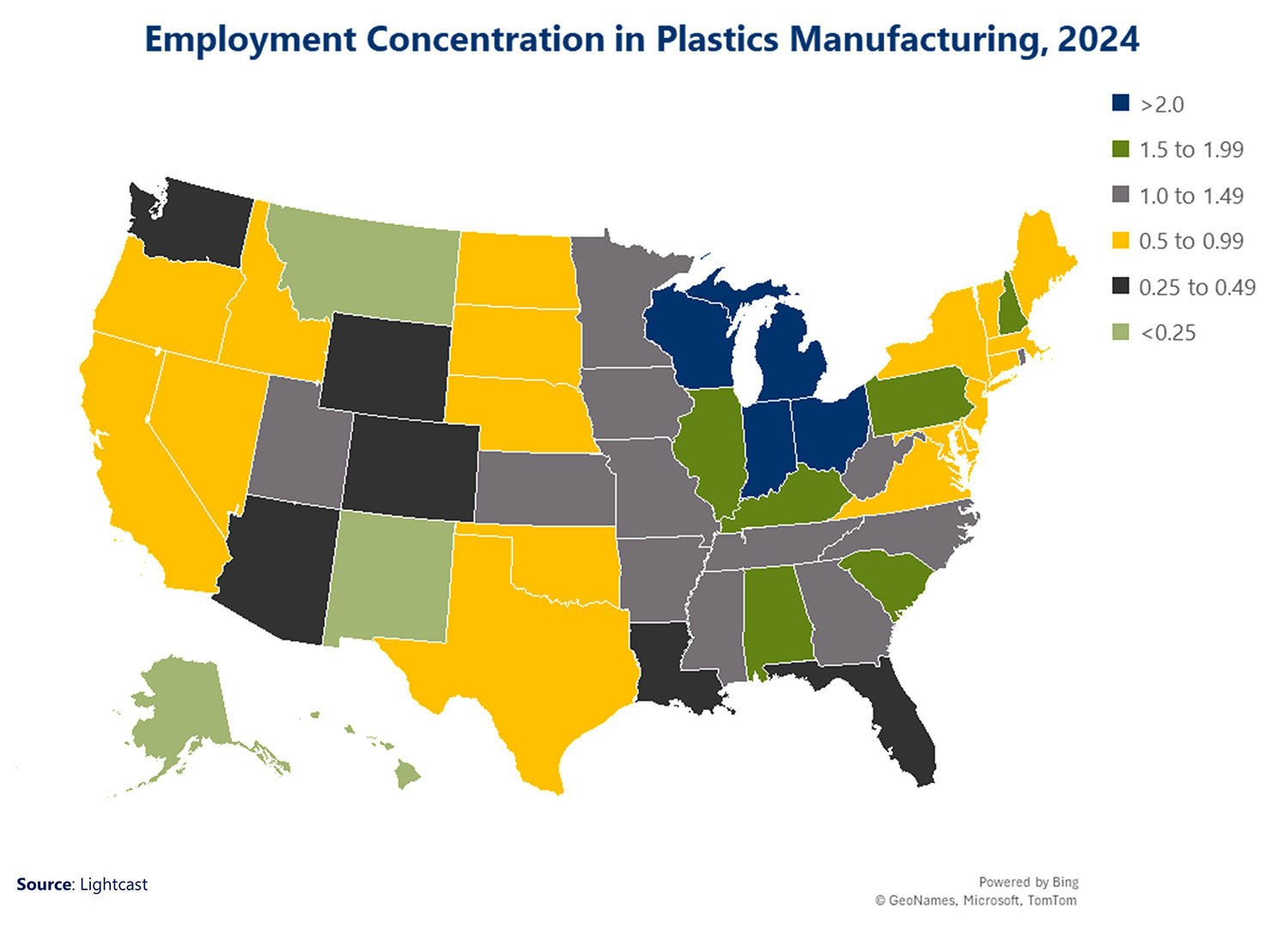

Wisconsin, Michigan, Indiana, and Ohio have twice the concentration of plastics manufacturing employment as the US. In Wisconsin and Indiana, for example, about 1% of total employment is in Plastics Manufacturing, compared to 0.3% of total employment for the nation as a whole.

Overall, concentration in Plastics Manufacturing is in line with the Midwest’s historical manufacturing legacy. Legacy manufacturing economies in Wisconsin, Indiana, Ohio, Michigan, Kentucky, Illinois, and Pennsylvania are among the nation’s leaders, alongside states like Alabama, Kentucky, and New Hampshire.

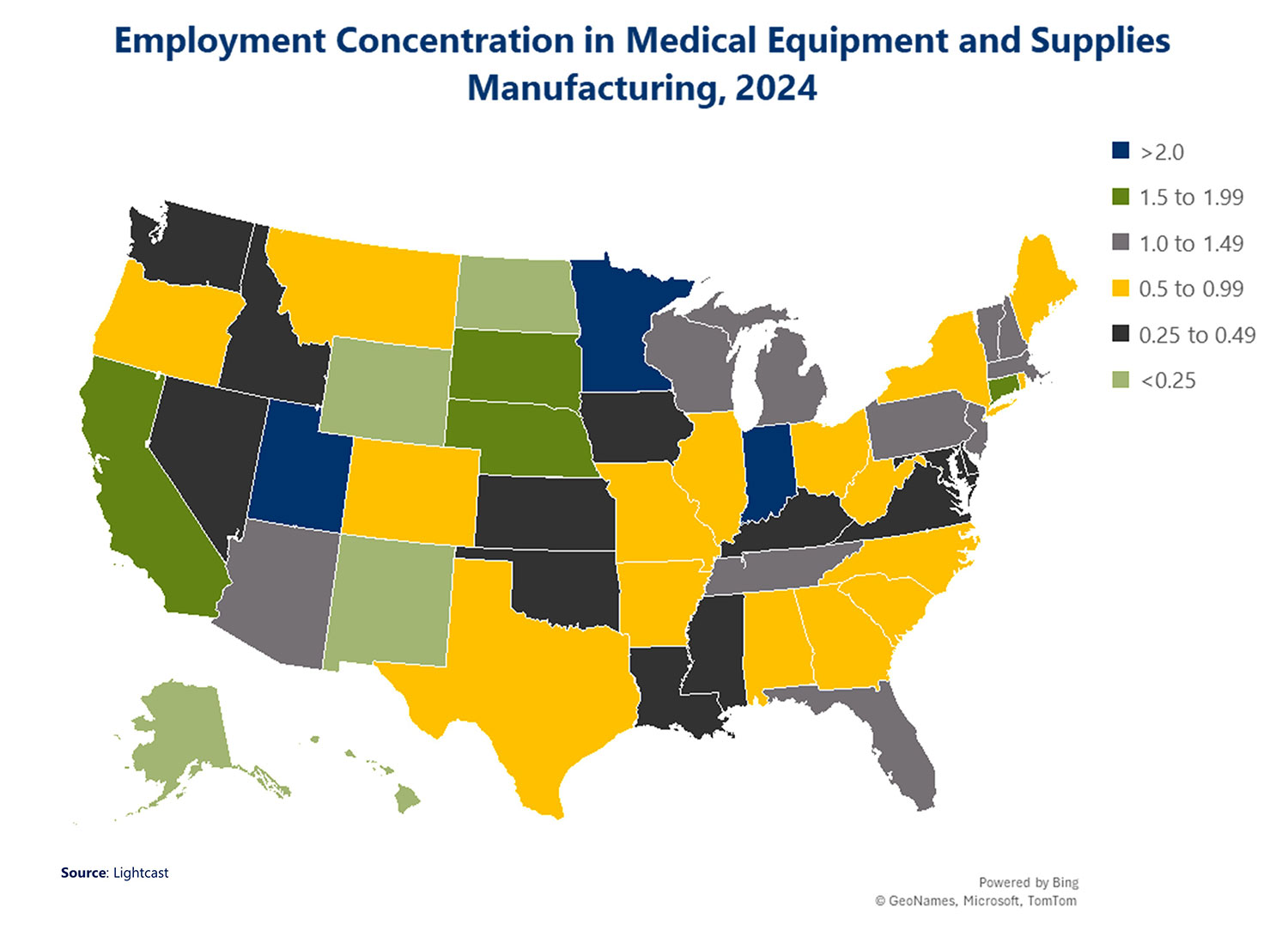

Utah, Minnesota, and Indiana are twice as concentrated in Medical Equipment and Supplies Manufacturing employment as the US.

About 0.7% of Utah’s employment is concentrated in the Medical Equipment and Supplies Manufacturing industry, compared to 0.2% on average across all states in the US.

This article is just the first step in unpacking the layers of data needed to understand and address risk across industries in the US economy. While national trade data offers a critical starting point, it’s only one part of the picture.

For economic development organizations and professionals, the next move is to dig deeper—exploring county- or MSA-level data to assess the specific local and regional implications of industry shifts and trade policy changes.

Equally important is incorporating real-time intelligence from the ground. Conversations with local employers can reveal risks and opportunities not captured in national datasets. These insights highlight the strategic value of strong, ongoing relationships between EDOs and their business communities.

Proactively engaging with employers, especially those in vulnerable or trade-exposed industries, can help economic developers identify and address potential challenges before they escalate into crises.

At Camoin Associates, we believe that knowledge is power—and with the right data, economic development leaders can make informed decisions that support both resilience and growth. Whether your community is facing uncertainty or navigating stable times, we’re here to help you understand your risks, strengthen your position, and explore opportunities.

Need help building a business retention and expansion (BRE) program that supports this kind of proactive engagement? Here’s a resource to get you started: Build a Business Retention and Expansion Program.

Learn more about our business retention and expansion services

Learn more about our industry analytics and strategy services

Economic and Fiscal Impact Analysis

A recent analysis of a digital equity program in Westchester County, NY, revealed that it generated outsized economic benefits and return on investment for the community.

Business Retention and Expansion (BRE)

Industry Analytics and Strategy

Your resource for understanding today and looking toward tomorrow